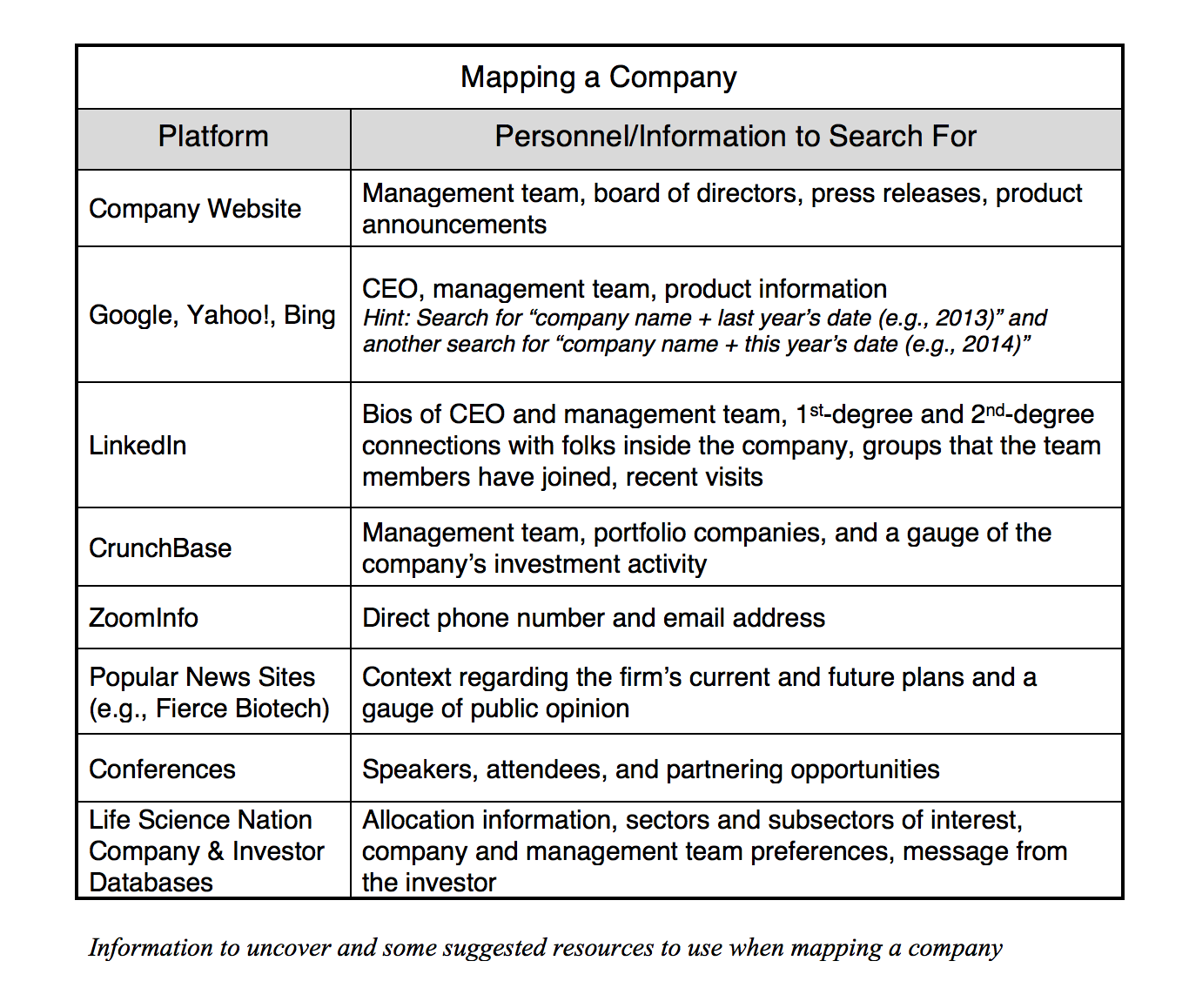

By Dennis Ford, CEO, LSN

After the launch of an outbound fundraising campaign, sooner or later a number of dialogues begin to take for with various investors. Meetings take place and relationships form. This is one of the most exciting parts of the fundraising process, and everything seems to be off to a great start. Unfortunately, this is also where many life science funding executives lead themselves astray.

After the launch of an outbound fundraising campaign, sooner or later a number of dialogues begin to take for with various investors. Meetings take place and relationships form. This is one of the most exciting parts of the fundraising process, and everything seems to be off to a great start. Unfortunately, this is also where many life science funding executives lead themselves astray.

Let’s face it; life science fundraising executives are beholden to a board, and they often feel pressure to put something on their forecast. Because they are anxious to turn a target into a prospect, they often begin to see things that aren’t there, try to force a fit, or use every skill they have to push along a relationship that isn’t going anywhere. It’s an easy trap to fall into, and can lead to a lot of unnecessary churn, eventually slowing down the fundraising process. You need to be equally focused on getting prospects on the plate and getting them off the plate. So how do you avoid being caught in this situation? Two easy rules can help you significantly.

Be direct: This is often a very hard thing for a fundraising executive to do, but it is a fundamental requirement in getting non-fits off the plate. Many entrepreneurs are so excited at the prospect of someone being interested in them that they are afraid to ask a question that could stop the dialogue. However, the alternative is wasting time on a non-fit. Always check in to see if the investor is actually interested in making an allocation, and ask what would prevent them from doing so. This will get every question answered faster and will get non-fits out of the conversation faster. This saves everyone time.

Listen to your gut. Opportunities can change direction, be postponed, stumble and fall off a cliff, and flat-out die. They are very tricky creatures. They prey upon your optimistic nature. They can get you in a fix. The importance of listening to your gut cannot be overstated. When in doubt, your gut will tell you what to do.

It’s imperative to concentrate on the good prospects and move on from investors who aren’t, pronto! It is also the reason to set everyone’s expectations at the outset of the process. Let those in your company know that a potential investor is ready for the forecast list only when you’ve made it halfway through the allocation process with them. A forecast list is composed of investors you have qualified who have also qualified your firm, and who may give you money. Stay focused, direct, and honest (with yourself). These are the key elements to efficiently navigating your way to an allocation.