By Michael Quigley, Director of Research, LSN

LSN researchers recently decided to take a deep dive into interviews we have held with venture philanthropy groups from around the world to see what the future likely has in store. After analyzing data gathered over the past three years from more than 150 investors, we uncovered a few notable trends.

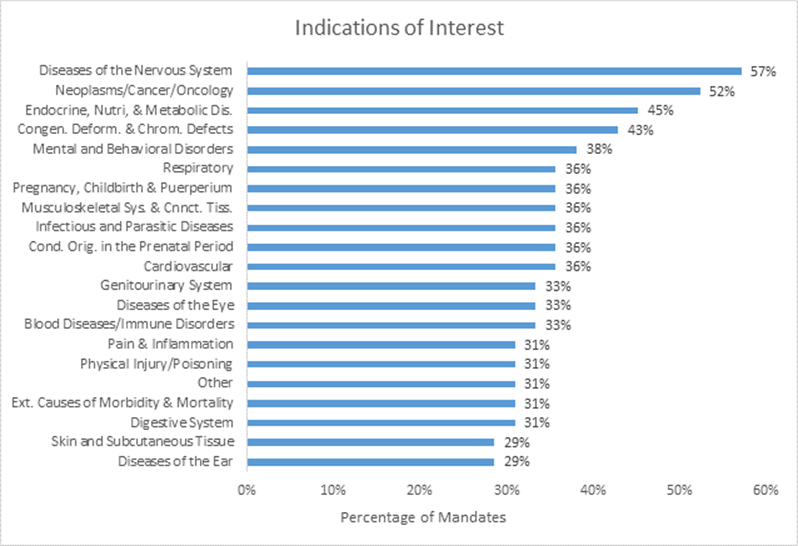

LSN researchers recently decided to take a deep dive into interviews we have held with venture philanthropy groups from around the world to see what the future likely has in store. After analyzing data gathered over the past three years from more than 150 investors, we uncovered a few notable trends.Diseases of the nervous system is the indication area with the greatest amount of interest from venture philanthropy investors. (See Figure 1.) This is likely a result of the notoriously high risk in this sector, stemming from a lack of accurate animal models that can serve as a viable gauge for human efficacy and safety. This heightened uncertainty drives many venture capital and other financially motivated investors away from the sector entirely, leaving a gap that venture philanthropy organizations hope to fill. Additionally, there are a massive number of unmet needs in the space, particularly with respect to diseases such as Alzheimer’s, the prevalence of which is increasing as the overall age of the population increases.

Figure 1 | Source: LSN Investor Platform, Data as of January 27, 2015

Oncology comes in second in terms of interest from venture philanthropy investors. Their interest is driven in part by the massive and growing need for improved treatment options in this indication area, particularly in orphan forms of cancer, some of which have foundations with venture arms that invest specifically in that field.

In third place, we have endocrine, nutritional, and metabolic disorders, driven by the number of diabetes-focused venture-philanthropy groups. And in fourth place, we have congenital deformities and chromosomal defects, also largely driven by foundations looking to fund companies targeting orphan diseases such as Duchenne muscular dystrophy, whose underlying cause can be tracked to genetic mutations.

Early Investments

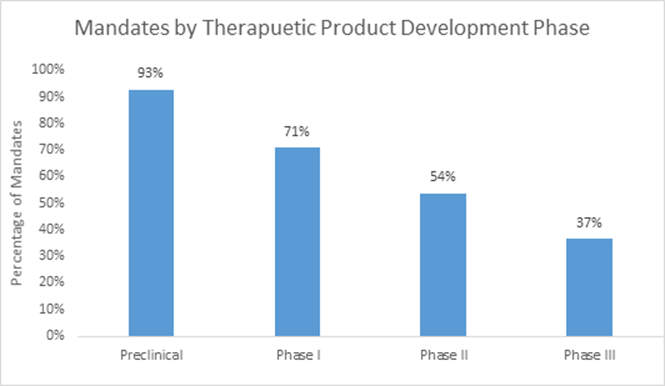

The largest percentage of venture philanthropy groups are looking to invest at the earliest phases of product development. (See Figures 2 and 3.) Other investors, and investors as a group, usually look for companies in Phase I of development for therapeutics and in the clinical stage for devices. However, because the primary motive of venture philanthropy investors is to improving patient care, they focus their efforts on the stages where capital is most lacking and innovation most prevalent.

Figure 2 | Source: LSN Investor Platform, Data as of January 27, 2015

Figure 3 | Source: LSN Investor Platform, Data as of January 27, 2015

Oftentimes, venture philanthropy investors view their allocations as a catalyst: an investment to help companies get the level of data required to become attractive to other institutional investors. Very few of these firms have the capital available to fund product development completely through commercialization; however, the capital they can provide in conjunction with their expertise and connections (to both providers and patients within the target area) makes these investors an invaluable resource to early stage companies.

Significant Allocations and Equity Positions

Another interesting metric to consider in the venture philanthropy landscape is the size and types of funding from these groups. (See Figure 4.) With nearly 50% of all venture philanthropy investors LSN has spoken with looking to make allocations of $1 million or more, it becomes clear that these groups are providing significant funding. Historically, these types of organizations have focused on financing academic and industry research through smaller grants and other forms of nondilutive funding. However, after years and years of their previously funded technologies not making it to the bedsides of patients, many have taken the challenge of funding research to a larger scale to deliver a more significant impact on patient care.

Figure 4 | Source: LSN Investor Platform, Data as of January 27, 2015

The foundations that have begun to dive into this realm of venture philanthropy do not look to provide purely nondilutive funding, however. More than 75% of the venture philanthropy investors we have interviewed that are providing $1 million or more are looking to take an equity position in the companies they allocate to. Granted, they are likely going to offer more favorable terms than a financially motivated investor; however, they are looking for equity. The model we have seen most frequently is one of an evergreen fund structure, where the firm invests in companies, takes an equity position, and any return that comes from those investments is then recycled back into the fund, allowing the group to further advance the standard of care in their indication.

Venture philanthropy is definitely of growing significance in the early stage of the life science investment ecosystem. As these groups evolve and new models for advancing care become utilized, it is highly valuable as a fundraising entrepreneur to be aware of all the players relevant to your technology. Given that they are capable of providing expertise, patients, invaluable connections, and, more recently, significant amounts of capital, companies that form strategic relationships with relevant philanthropic groups can undoubtedly be served well in most aspects of development.

NextPhase has published numerous articles on venture philanthropy funding. You can find them on our website here and here.

Leave a comment