By Lucy Parkinson, Senior Research Manager, LSN

Two weeks ago, we took a dive into early stage life science assets in the Southwest region of the U.S. Today, we’ll take a look at what’s happening closer to our home, here in the global life science hub of the Northeast.

Two weeks ago, we took a dive into early stage life science assets in the Southwest region of the U.S. Today, we’ll take a look at what’s happening closer to our home, here in the global life science hub of the Northeast.

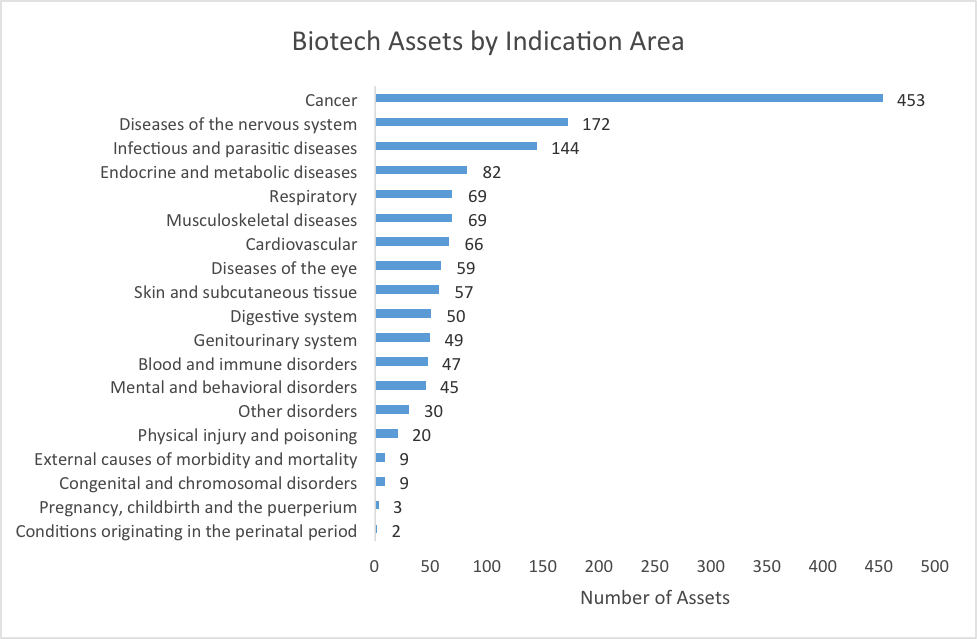

Using the LSN Company Platform, we are able to observe the wealth of innovation occurring in this region. We analyzed a sample of biotech and medtech innovators across nine Northeastern states: Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, and Vermont. This sample drew from the pipelines of almost 400 life science companies, and included 1596 biotech assets in a range of developmental phases, from Preclinical through Phase III trials, as well as 154 medtech products in development. For 1435 of the biotech assets, we are able to track the primary indication area targeted by the product, as is shown in Figure 1. As in the Southwest, we saw significant pipelines in cancer, diseases of the nervous system, and infectious and parasitic diseases. With such a large sample, even less crowded indication fields such as blood and immune diseases and mental and behavioral disorders possess a significant number of pipeline assets.

Figure 1 | Source: LSN Company Platform, Data as of March 11, 2015

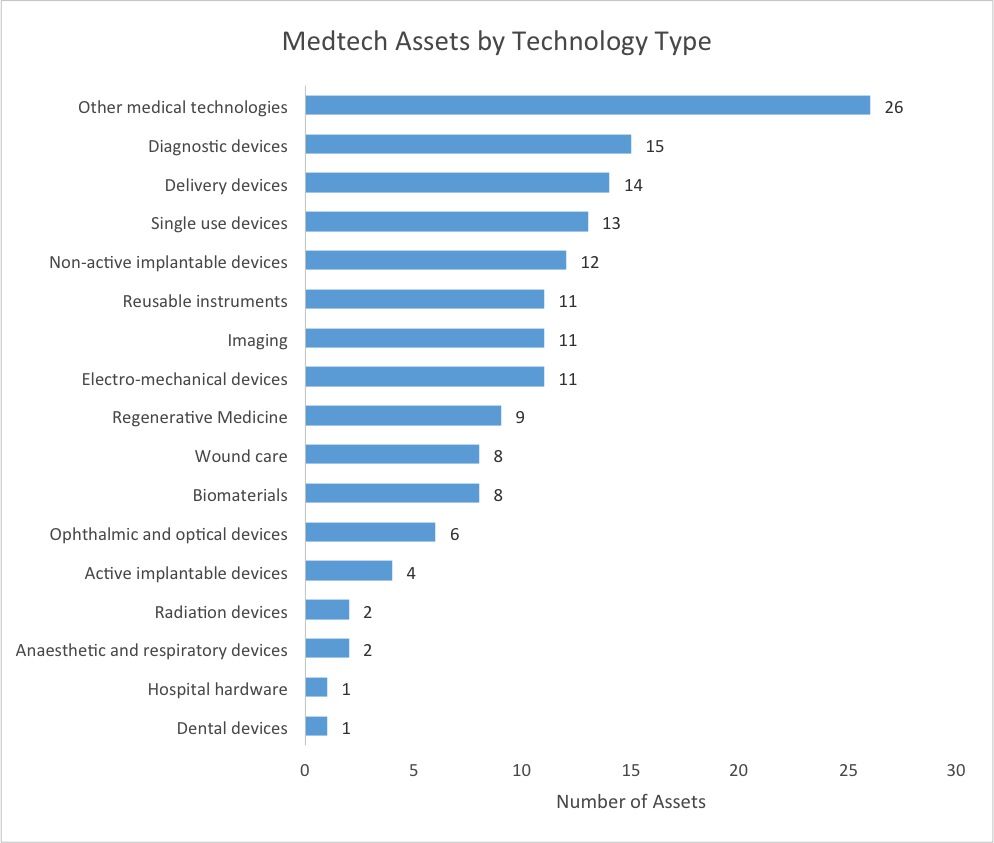

We also found a great variety of medtech assets, as is shown in Figure 2. Diagnostic devices and delivery devices were the two most common technology types; this is in sharp contrast with the Southwest, where implantable devices and reusable instruments were the leading fields of medtech innovation.

Figure 2 | Source: LSN Company Platform, Data as of March 11, 2015

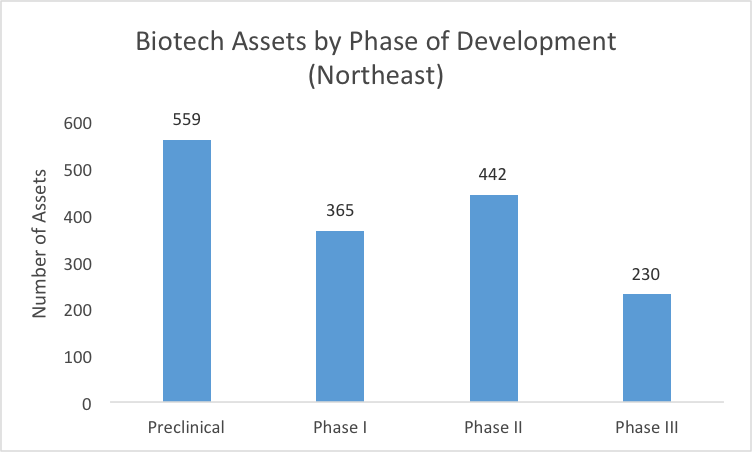

Of the biotech assets, the greatest number are at the preclinical phase of development. However, Figure 3 shows that the drop-off before the IND is much less sharp than we saw in the Southwest.

Figure 3 | Source: LSN Company Platform, Data as of March 11, 2015

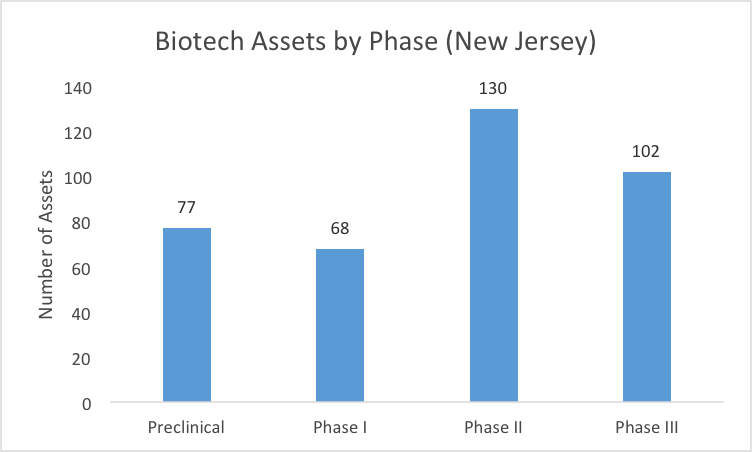

There are fewer than 2 preclinical assets for every Phase I asset, and only 2.4 preclinical assets for every Phase III asset. This is likely because the local pharma strength leads to assets migrating to the region as they progress through the pipeline due to relocations, partnerships, or acquisitions. One notable state within the sample is New Jersey (see Figure 4), where we find more Phase III assets than preclinical or Phase I assets.

Figure 4 | Source: LSN Company Platform, Data as of March 11, 2015

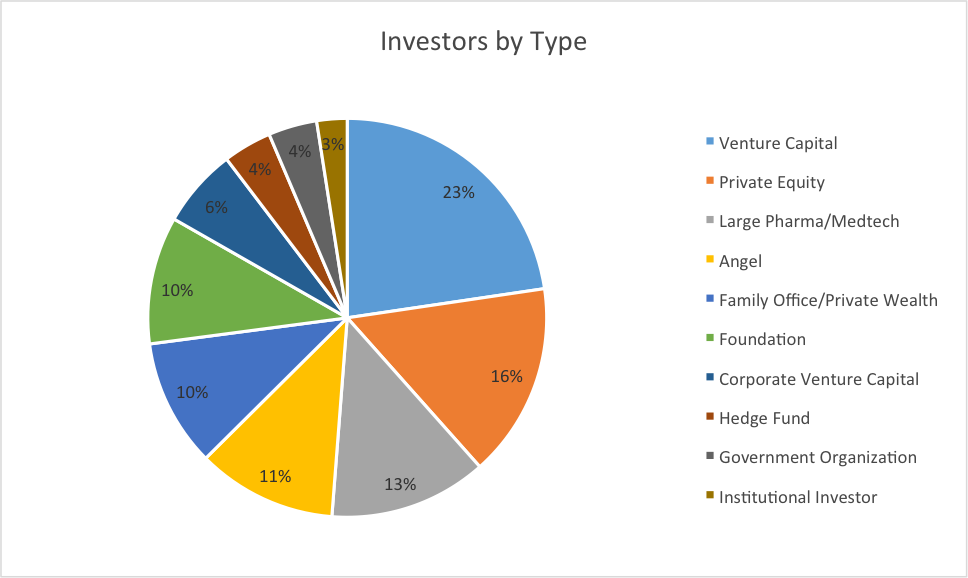

As the Northeast is well-known for life science innovation, it’s unsurprising that we also find many local investors who are interested in early stage life science opportunities. Figure 5 shows the types of investors that LSN has identified in this region.

Figure 5 | Source: LSN Investor Platform, Data as of March 11, 2015

There are significant distinctions between life science investors in the Northeast and life science investors in the Southwest. Predictably, we see a greater corporate presence, with large pharma and medtech companies and their corporate venture funds together comprising 19% of active life science investors in the region. Only 23% of Northeast-based life science investors are venture capital firms, a clear sign that it’s important to look beyond this funding source if you’re seeking a Northeast-based investor.

Leave a comment