By Jacob Setterbo, Director of Grants, HIREtech

Startups can now benefit from both grants and R&D Tax Credits

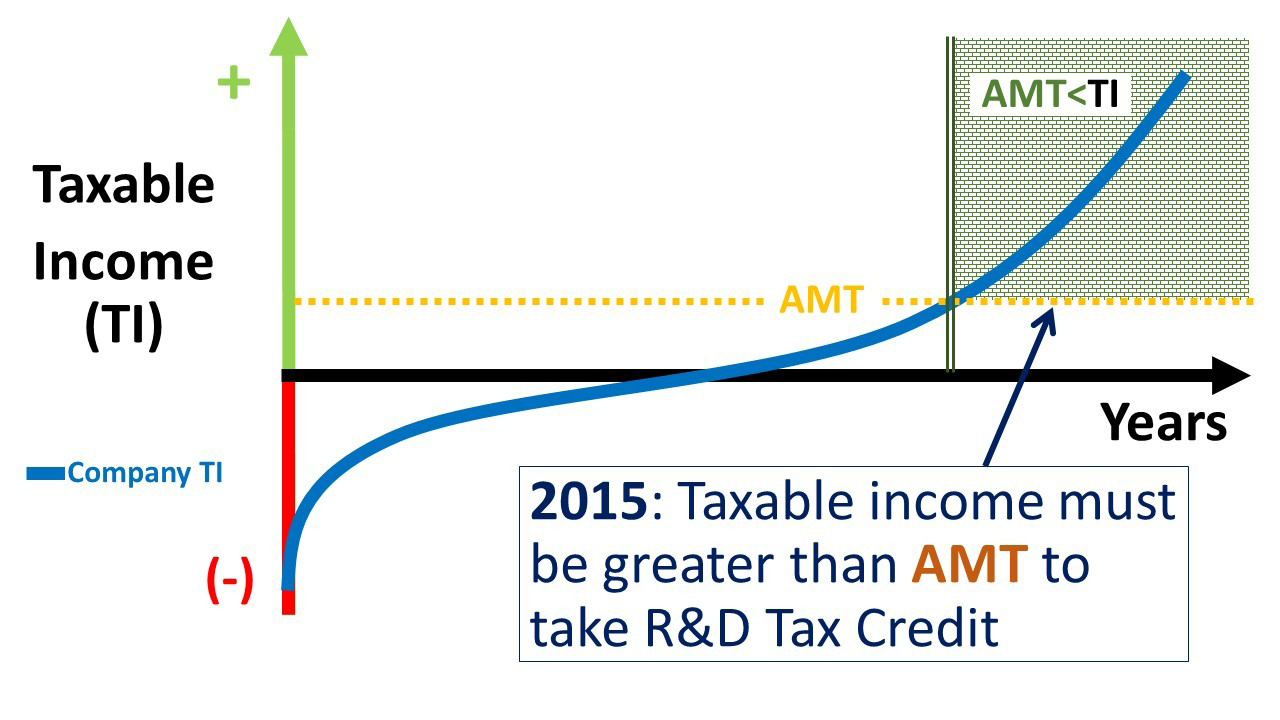

The R&D Tax Credit was created by Congress to encourage R&D investment within the United States. In the past, however, R&D credits were only available to companies that are profitable, as companies that have yet to turn a profit had no tax burden to be reduced by the credits. It seemed unfair that life science startups, which primarily perform R&D but typically pay no income tax for years, could not benefit from the R&D Tax Credit (FIGURE 1).

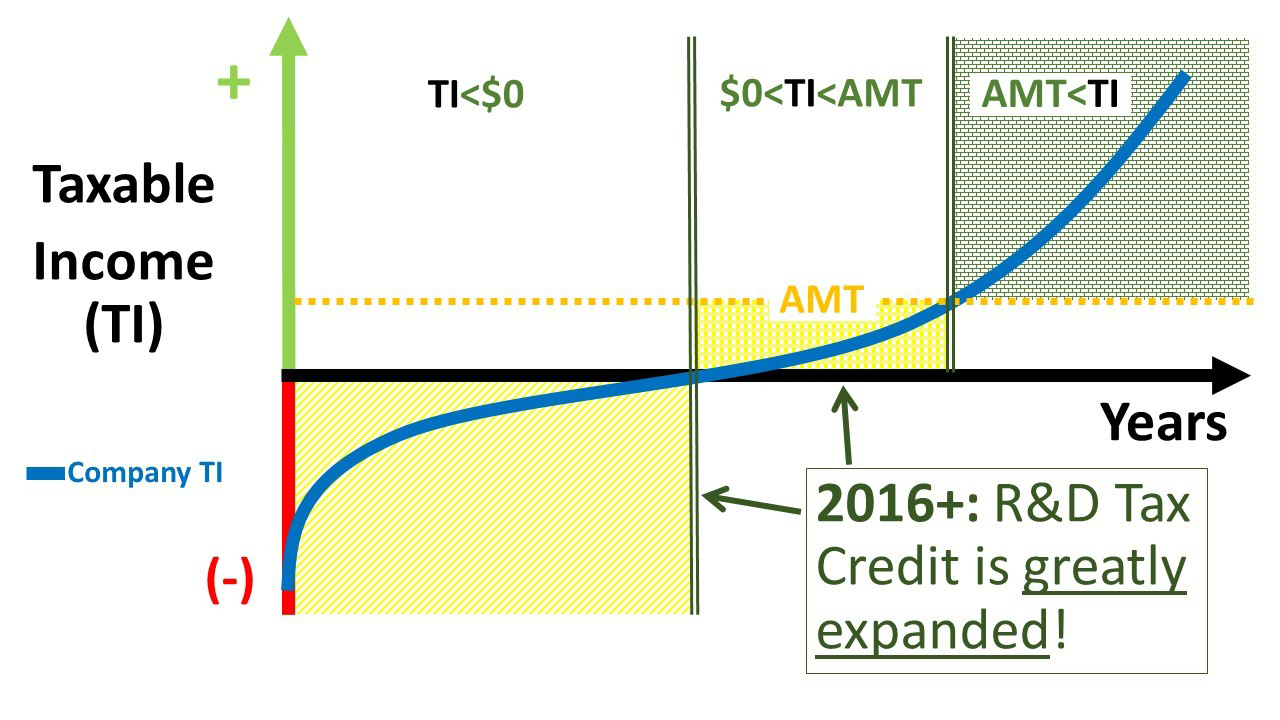

This disparity between profitable companies and startups has finally been resolved, and startups can finally benefit from R&D Tax Credits. The gap was closed by the PATH Act, signed on December 18, 2015 (FIGURE 2). In addition to making the R&D Tax Credit permanent and allowing it to be applied against the Alternative Minimum Tax (AMT), the PATH Act allows startups to use the R&D Tax Credit to offset payroll taxes for up to 5 years. This change is particularly beneficial for life science startups, because it often takes several years before their income exceeds their expenses. Plus, everyone has to pay payroll taxes!

Grants and tax credits are similar in that they are non-dilutive (you don’t lose equity) and you don’t have to pay them back. Their main difference is that grants are forward-looking whereas tax credits are backward-looking. For grants, you have to convince reviewers (often professors) that your proposed future project is significant, innovative, and will have a great impact on public health. The national “success rate” for SBIR/STTRs is typically somewhere around 15-20%. For tax credits, you just have to be able to prove that you performed R&D the previous year. While you must confirm your eligibility, understand what is considered “qualified research expenditures,” and know how to calculate the credit, I can assure you that the “success rate” for R&D Tax Credits is near 100% if you follow the rules.

As a life science entrepreneur, it is in your best interest to seek various funding sources. Grants are an excellent source of non-dilutive funding that can push your project forward, but, as noted on www.sbir.gov, they are “highly competitive.” Fortunately for startups, the new R&D Tax Credit rules allow you to offset your payroll taxes if you perform R&D in 2016. Like grants, these tax credits are non-dilutive, but, unlike grants, they are nearly a sure bet when calculated correctly.

Jacob will be presenting an upcoming RESI Workshop on R&D Tax Credits at RESI@TMCx in Houston on April 11. View the full RESI agenda here.