As RESI prepares for its second landing on MaRS on April 4th, the team at Life Science Nation is proud to announce the RESI investor panel agenda. With three tracks of panel and workshop content, RESI will feature a wealth of speakers representing all categories of life science investors, from family offices to VCs and angels to big pharma. These panels are a must-see for any fundraising entrepreneur in the sector.

New to Toronto this year LSN will be bringing our latest and highly popular Asia-North America Panel Track, featuring 15 speakers representing Asia based firms seeking to invest in and/or acquire North American life science companies. Entrepreneurs can hear from real investors who are driving the increase in transpacific investments. See if your technology fits their mandate!

We are excited to be bringing these diverse investor groups into the flourishing innovation hub of Toronto and granting them a unique look into Canada’s innovative healthcare scene. Stay tuned for updates as we continue to confirm speakers and announce panels.

On April 4th, the Redefining Early Stage Investments (RESI) Conference will be held at the MaRS Discovery District for the second time. RESI is a full day partnering event that allows early-stage life science, med tech, and digital health companies meet and develop relationships with investors and strategic partners all within the heart of Canada’s healthcare innovation hub.

“It was unique in that it allowed us, in a short period of time, to connect with potential investors, potential clients, folks in the ecosystem we already knew, and new folks we wanted to meet.” – Raymond Shih, President & Co-Founder, QOC Health

Due to the success of last year’s conference RESI (500 attendees, facilitating over 800 meetings between companies and potential investors and partners) this year the conference will be held during Toronto’s Health Innovation Week.

Catch a glimpse into the RESI on MaRS Conference in the video below, and be sure to register for RESI@MaRS for a chance to dive straight into Toronto’s Health Innovation scene!

Orphan diseases present a unique opportunity for an investor as there are several advantages from a regulatory standpoint given the shorter development timeline and exclusivity possibility as well as the ability to truly impact patient’s lives that have no treatment options. On the flipside, they have challenges primarily due to the size of the patient population and usually require a somewhat unique business model and marketing strategy to be a viable opportunity.

In our first and largest RESI conference of 2017, held for the third time at the Marines Memorial Club and Hotel during the JP Morgan healthcare week, a varied group of investors explore some of these challenges and opportunities with funding and commercializing rare disease drugs and share their firsthand experience in this space.

Moderated by Ken Kengatharan, General Partner, Atheneos Capital, panelists include:

By Mary Gooderham, on behalf of MaRS Discovery District

Health investors from the United States are discovering vast prospects in Toronto as a hot-spot for biotech innovation and a place to invest in cutting-edge life sciences startups.

To Jerel Davis, managing director of Versant Ventures, the global venture capital firm behind recent landmark deals in the city, “Toronto is pretty remarkable,” as a “completely under-tapped” market with strengths in fields ranging from regenerative medicine and oncology to heart disease, children’s health, radio medicine and imaging.

“The opportunity is huge,” he says, noting that U.S. capital and large pharmaceutical companies are attracted by Toronto’s capacities “across the board” in science and healthcare delivery. “There’s a very strong cluster of hospitals and research institutes in a very concentrated area. Many of them are top in North America, if not the world.”

The ease of access to those capacities is equally exciting, he says, with lower competition in the emerging ecosystem allowing VCs “willing to do the hard work and roll up their sleeves” to tap into fundamental science, working with the best academics in their fields.

One indication of the growing interest in Canada’s healthcare scene is the number of investors drawn to the annual Redefining Early Stage Investments (RESI) on MaRS conference. The largest health investor event in Canada, it is set to take place on April 4 (followed by the MaRS HealthKick Challenge on April 5). Davis attended last year’s event and says it allows VCs to quickly scout and assess top Canadian health companies. “It brings together in one room all the key players driving innovation in the health sector—VCs, angels, startups, academics and corporates—and facilitates finding the most disruptive ideas.”

Recent data on venture capital investments in the sector also point to increased momentum. According to CB Insights, VCs invested over $596 million in Canadian life-sciences companies in 2016, the most on record in a single year and almost 100 per cent higher than all of 2014.

Multinationals joining the Canadian health scene include Bayer, Celgene, Johnson & Johnson and Novartis, Davis says: “The list goes on and on and on.” Versant was involved in one of the biggest deals to take place in 2016—the second-largest initial investment in a startup in the history of the biotechnology industry—joining Bayer to invest $225 million U.S. to create BlueRock Therapeutics, a new company with significant operations at MaRS that will commercialize regenerative medicines from stem cell research.

Davis says that MaRS “serves as an important beacon,” from its critical development infrastructure to introducing foreign investors to the Toronto scene. In fact, since the Versant-Bayer deal last December, two other big announcements involving Toronto-based health startups in the MaRS network have been made: Highland Therapeutics raised $200 million to shake up the multi-billion dollar ADHD drug market; and Meta, a startup that provides an AI-powered search engine for researchers and doctors, was the first purchase made by the Chan Zuckerberg Initiative for an undisclosed amount.

Mary Haak-Frendscho, a venture partner at Versant and CEO of Blueline Bioscience, which is also based at MaRS and acts as the Canadian discovery engine for Versant, says that “MaRS is the centre of the hub and a key component of the ecosystem…You have everything right there, you have the entrepreneurs, you have the science, you have the clinical research for translation.

“The venture community is uniquely poised to fill the Canadian gap; everything is ready for them to step in,” Haak-Frendscho says, pointing out that pharmaceutical companies are also increasingly involved. The recent increase in the size of investments in the Toronto market reflects the quality of science and innovation in fields such as regenerative medicine and neurosciences.

“I’m sensing a turning point here and it’s pretty exciting,” she says. “There are cool things going on in Canada, in Toronto. When you have solid deal flow that is at a globally competitive level, people pay attention.”

Toronto is a test-bed for new business models that bring together VCs and big pharma to pool investments that speed up development. Davis says these include a “build-to-buy” approach, where partners help originate companies with an option to acquire them, while “other creative options continue to emerge,” including approaches where pharmaceutical companies like Celgene move in earlier to get access to technology and “bold collaborations” like the BlueRock deal.

“We want to accelerate innovation,” he says, adding that Toronto is an “obvious hub” in which to do it.

To learn more about the RESI on MaRS conference and to register, click here.

Big pharmaceutical companies have been a major player in the life science investment space for decades, yet historically they have been known to “just license, and say goodbye.” Today, these large corporations have taken new partnership models in the form of smaller funds set aside, innovation centers, and the like. Strategies and approach to these strategies have been changing in the last 5-7 years. With 40-60% of successful assets having come from external opportunities, it is with great note that big pharma is very closely following and adapting along the trends within the biotech ecosystem.

On January 10th, LSN gathered five highly experienced big pharma representatives for the Redefining Early Stage Investments panel in San Francisco around JPM. Moderated by Barbara Sosnowski, Vice President, External R&D Innovation, WRD of Pfizer and panelists representing Johnson & Johnson, Gilead, and Amgen shared insights around these trends in a variety of topics well-recommended for entrepreneurs and players in the space to take careful note.

Transformative Science is Worth Looking At, Though It’s An Upstream Battle

While all big pharmaceutical companies have their strategic angles – oncology, cardiovascular/metabolic, neuroscience, inflammation, to name a few – panelists added that, to be truthful, if the science is compelling enough, they will look at it.

“It’s all about influencing change,” Jeremy Grunstein, Executive Director of BD at Amgen, began. “The reality is, if you have something that makes a major difference for an unmet disease, that’s something that ought to be interesting to everybody.”

Sosnowski added that her team will definitely assess these disruptive technologies, but “it’s like a salmon swimming upstream” to put it through the governance process, due to its strategic misalignment. “But if the science is so compelling that it could be a game-changer, I think it’s worth the energy to swim upstream and get it through the senior leaders.”

Carolyne Zimmermann, Senior Director in Transactions at Johnson & Johnson described that a process “swimming upstream” would require heavy lifting and will require contacts within the pharma to champion the technology. Champions or not, Zimmermann added the importance of a contact who can articulate the pharma’s activity level: “we are going to the review board, here is our committee process, the people involved, etc.”

It Takes Time for Market Assessment

Especially for technology outside of their core strategies, Sosnowski outlined the market assessment and target product profile to take at least six months overall – three months for qualitative assessment, and three months quantitative assessment. Sosnowski understands the time frustration from the biotech perspective, but she explained that assessment “must come de novo,” especially as a lot changes over time (market, competition). “If we communicate how long that’s going to take and you and we understand that, then we are all in line,” Sosnowski added.

There is an Emphasis in External Opportunities

If there is any doubt in the matter, the panelists assured the huge emphasis in scouting external opportunities. For Amgen, Grunstein stated 50% of their commercialized products came from licensing and M&A. For J&J, Zimmermann stated that 40% of assets going into Phase II or III were externally innovated.

“I hear 40%, 50%, even 60%,” Zimmermann exclaimed, “It’s that we recognized that external innovation is crucial in our ecosystem.” Furthermore, Zimmermann added that “smaller companies can move cheaper, faster, and better than larger organizations.”

Partnering Models

In the past, partnership models for big pharma had a habit to just in-license. “Thank you very much, we will take over the development,” Zimmermann mimicked. The panelists, however, noted that within the last 5 to 7 years, there has been a real change to how these big pharmaceutical companies are striving to “be more biotech-like. “

Sosnowski outlined Pfizer’s creative funding model that keeps the firm from “just licensing.” Part of the strategy includes a seed fund, which acts as a convertible debt to pre-Series A companies to support the companies to be validated and off the ground. “It’s a great way to get in early and help guide the company moving forward… [and] think more creatively and out-of-the-box to how we can get earlier where there is higher risk.”

Zimmermann added the reasoning behind this outlook: “What I see emerging is the recognition that the entrepreneurs are deeply embedded in this particular science and are world-class leaders in that science.” She further elaborated that working with the entrepreneur by providing advice and resources may even be a better way to collaborate than a traditional license deal.

Monica Viziano, Senior Director, Alliance Management at Gilead Sciences explained that the in-licensing model is not scalable, “Licensing and complete control is a limitation in what we can even do. There is a recognition that we have to move on with a big change in mentality, particularly in R&D.”

Final Advice

Send your data – “We all know there are unknowns, but there are also established preclinical models in therapeutic indications,” said Zimmermann. Furthermore, if you have a novel asset, “show that your drug is working in the way you think it is with some mechanism of action data,” added Grunstien. Sosnowski outlined receptor engagement, how much coverage you will need, and specificity of target as major points to address.

Focus your material – “Be able to put it in a framework and story. If [the technology] is asset A, then don’t spend time talking about BCD,” described Viziano.

Have a conversation rather than email – “You can get a lot more from a conversation than an e-mail,” said Zimmermann. “Pick up the phone or find them in the next conference.” Sosnowski added that coming from her biotech background, she works hard to address feedback as thorough as possible.

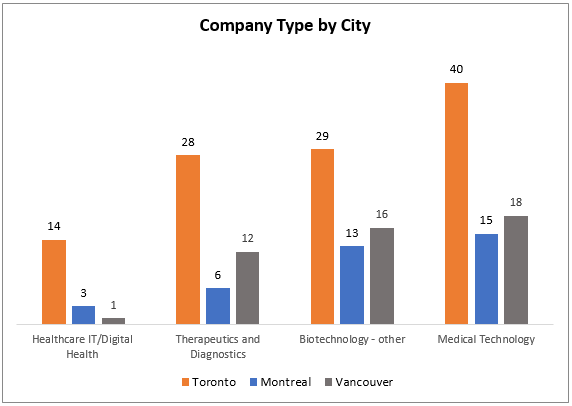

Taking a sample of Canada data from the LSN Company Platform, we can assess the most popular sectors for life science startups in Canada’s top three most populous cities.

Medtech was the most represented sector. There are a couple of different possible reasons for this: 1) medical technology is a fairly broad term and there tends to be some overlap with digital health given that underlying a lot of medical devices, primarily the newer ones, is a software component; 2) generally speaking, the amount of capital required from inception to commercialization for a medical device tends to be considerably less than for a biopharmaceutical product due to fewer and smaller clinical trials, and given that there are less venture and corporate dollars available for Canadian startups as compared to the U.S., entrepreneurs pursue less capital-intensive opportunities.

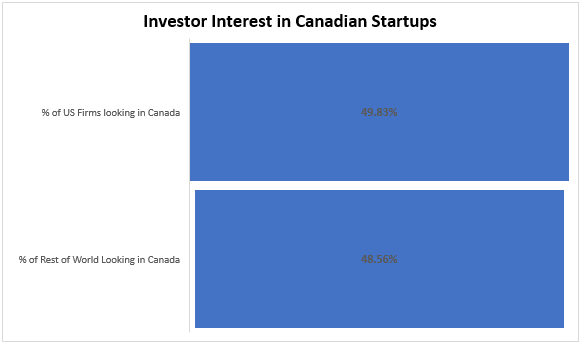

Taking a look at the LSN investor platform, the below data shows the percentage of investors in the U.S. and the rest of the world (excluding Canada) that have stated they are actively looking for technology in Canada.

One thing we hear over and over from early-stage investors, particularly those based in the US East Coast or Silicon Valley, is that Canadian startups are attractive due to their reasonable valuations, as compared to valuations in traditional life science hubs such as Boston and San Francisco. Some U.S.-based investors are going as far as setting up offices in Canadian cities to take advantage of this fact. In addition, well-established VCs in the U.S. hubs see just about every deal out there, and are increasingly looking for innovation in less saturated areas. About half of the U.S. investors and investors in the rest of the world that are tracked by the LSN research team are looking to invest in Canadian startups.

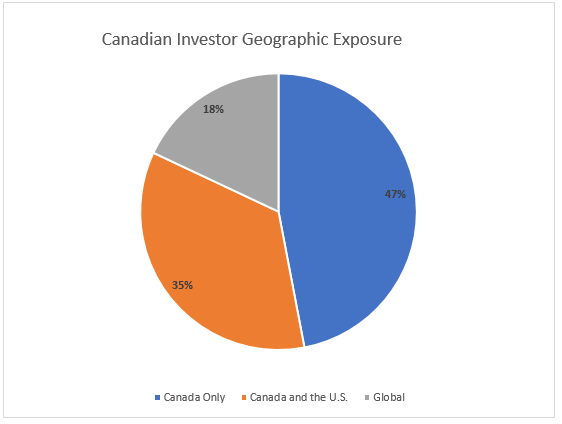

As for the Canadian investors, about half of them are putting money to work only in their own country.

We’re excited to bring the RESI conference back to Toronto for a second time and get a firsthand look at the innovation that is happening in this rapidly developing life science hub, as well as expose the technologies to a diverse group investors and strategic partners.

2016 has been a mixed year for pharma, with new drug approvals well down from the 2015 highs, but major pharma firms continue to search outbound for the drugs of the future. The LSN Licensing Deals Platform provides detailed information on announced pharma deals, and this data allows us to take a look at the overall dealmaking landscape in 2016.

The LSN Licensing Deals platform doesn’t include M&A, and only covers deal announcements in which some financial information was stated, such as upfront and milestone payment amounts and/or a royalty percentage. In 76% of cases, the data includes an upfront payment amount; these varied considerably, with some preclinical deals providing under $1 million in immediate cash, and some Phase II and Phase III deals bringing in hundreds of millions.

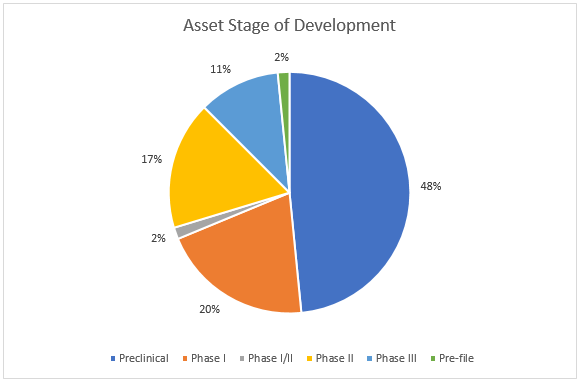

Most 2016 Deals Were Preclinical

Among deals in which an asset stage of development was stated, preclinical assets were by far the most common, featuring in almost half of these deals. This figure has shot up since 2015. In an increasingly competitive arena, major pharma firms inked deals early.

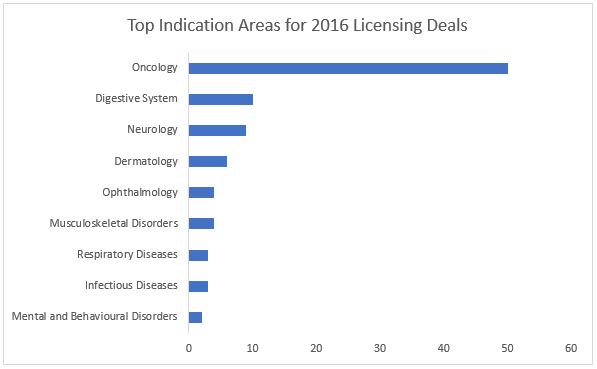

In deals in which a single specific disease area was identified, oncology opportunities predominated, exceeding other major fields of medicine by several times over. In surprise second place came the digestive system, with a 50% increase in reported deals over 2015. Other popular fields include neurology, dermatology, ophthalmology and musculoskeletal disorders.

Both New Innovations And Mainstays Attract Deal Interest

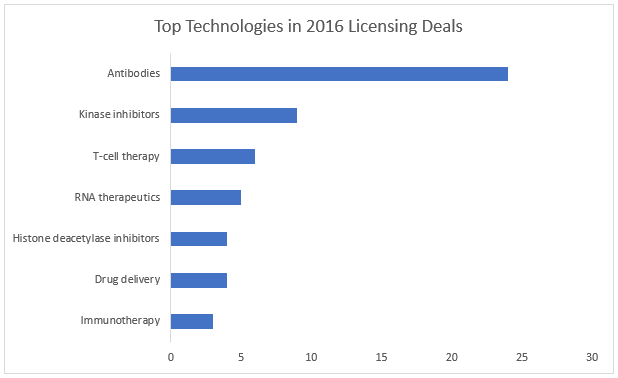

For many deals, the LSN Licensing Deals Platform describes the type of technology involved in the transaction. Some are widespread, while others are in a class of their own. There’s still a considerable amount of interest in antibody innovations, with over 20% of all deals involving an antibody. Antibody technologies were primarily either monoclonal or bi-specific antibodies, with several other types of antibody technologies being shopped, such as antibody-drug conjugates.

T-cell technologies (including CAR-T) continue to attract interest. However, so do kinease inhibitors, proving that this small molecule approach is not yet ‘yesterday’s science’ . Other technologies that remain sought after include RNA therapeutics and drug delivery technologies.

There’s A Lot Of Fish In The Sea

As ever, you won’t be surprised by the names of the most prolific licensees in the dataset (it’s evens between Roche, Merck and Bristol-Myers-Squibb, with other well-known global pharma firms very close behind them). However, over 70 pharma firms, located in every corner of the globe, announced a licensing deal last year. If you’re looking for a strategic partner for your asset, it’s worth hunting beyond the top 10 or even top 50 largest firms. The LSN data platforms provide detailed information on potential development or exit partners far outside that mainstream.

The firm is focused on therapeutics companies and does not invest in medical devices, diagnostics, or digital health. The firm is open to considering assets of very early stages, even those as early as lead optimization phase. The firm considers various modalities, including antibodies, small molecules, and cell therapy. Currently, the firm is not interested in gene therapy. Indication-wise, the firm is most interested in oncology and autoimmune diseases but has recently looked at fibrotic diseases and certain rare diseases as well.

The firm is opportunistic across all subsectors of healthcare. Within MedTech, the firm is most interested in medical devices, artificial intelligence, robotics, and mobile health. The firm is seeking post-prototype innovations that are FDA cleared or are close to receiving clearance. Within therapeutics, the firm is interested in therapeutics for large disease markets such as oncology, neurology, and metabolic diseases. The firm is open to all modalities with a special interest in immunotherapy and cell therapy.

A strategic investment firm of a large global pharmaceutical makes investments ranging from $5 million to $30 million, acting either as a sole investor or within a syndicate. The firm is open to considering therapeutic opportunities globally, but only if the company is pursuing a market opportunity in the USA and is in dialogue with the US FDA.

The firm is currently looking for new investment opportunities in enterprise software, medical devices, and the healthcare IT space. The firm will invest in 510k devices and healthcare IT companies, and it is very opportunistic in terms of indications. In the past, the firm was active in medical device companies developing dental devices, endovascular innovation devices, and women’s health devices.

A venture capital firm founded in 2005 has multiple offices throughout Asia, New York, and San Diego. The firm has closed its fifth fund in 2017 and is currently raising a sixth fund, which the firm is targeting to be the largest fund to date. The firm continues to actively seek investment opportunities across a […]

Health investors from the United States are discovering vast prospects in Toronto as a hot-spot for biotech innovation and a place to invest in cutting-edge life sciences startups.

Health investors from the United States are discovering vast prospects in Toronto as a hot-spot for biotech innovation and a place to invest in cutting-edge life sciences startups.