By Phubes Asavasatitporn, Research Analyst, LSN

At LSN, we talk a lot about having an “up-to-date roadmap” when it comes to navigating the changing life science investment landscape. This means not only understanding who the new entities in the space are, but also how their investment strategies have changed, what type of technology each is interested in, how their investment timelines have been reconfigured in the churn, and so on. One topic that is less frequently taken into account, however, is the idea of actually mapping out an individual investment firm before a big meeting.

At LSN, we talk a lot about having an “up-to-date roadmap” when it comes to navigating the changing life science investment landscape. This means not only understanding who the new entities in the space are, but also how their investment strategies have changed, what type of technology each is interested in, how their investment timelines have been reconfigured in the churn, and so on. One topic that is less frequently taken into account, however, is the idea of actually mapping out an individual investment firm before a big meeting.

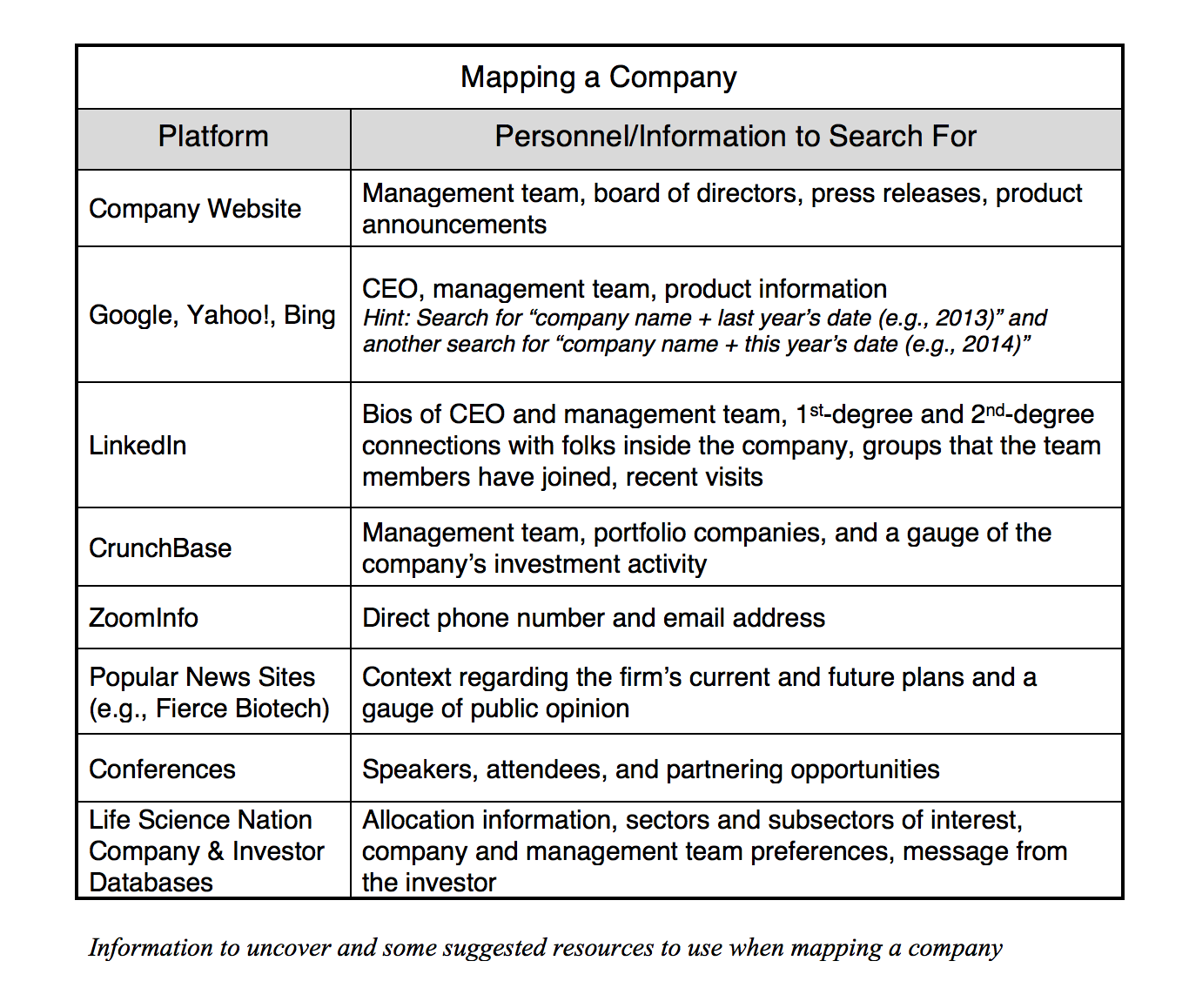

Fundraising executives will handle the process of mapping out a company in different ways based on a variety of variables – not the least of which is personality type. Some like to approach the problem much like a case study, spending weeks doing research on the prospect (and their peers’) management team, portfolio companies, investment interests and past deals. Others may prefer to simply go in with a general idea of a firm’s investment category, and then gather the rest of the relevant information first hand. Either tactic has its advantages, and more than likely, your actual efforts to plan for an initial meeting with an investor will be some combination of the two.

While the investigative angle helps you to align your perception with prospective investors as prepared and informed, and may lend itself to stronger long-term relationships, it does have its drawbacks. For one, a fundraising executive’s primary goal should always be towards creating as many qualified investor relationships as possible. For this reason, spending too much time researching targets – and therefore not enough time making calls or knocking on doors – is taking away from the main task at hand. Incremental to this is the fact that too much research can lead the focus of a meeting towards verifying data and away from actually talking with the prospect. The key is striking an effective balance.

None of this is to say that data shouldn’t be verified, because it must. On the other hand, one of the worst mistakes an executive engaged in the fundraising process can make is to assume that their initial research on an investor entity was 100% correct. Information – especially regarding corporate structure and hierarchy – is constantly in flux. Indeed, it is hard to gauge how much time you should allocate to researching your prospects, but some general rules are to not mistake “less” for “none,” and try to find a happy balance between “too much” and “not enough.”

Whatever approaches you do take to investor meetings, keep in mind that the most important piece of any meeting is to lay the groundwork for a good relationship. Too many entrepreneurs make the mistake of believing that technology is not only the most important part of a deal, but the only piece that really matters. On the contrary, it is real conversations that lead to real relationships, and real relationships that lead to allocations. Do – but don’t overdo – your due diligence on your prospective investors, and approach each situation with a confident and friendly demeanor, and with enough attempts, the correct fit will eventually come along.