By Jack Fuller, Investor Analyst, LSN

A recent report that took a look at the current trends and future forecasts for drug development found that compared to conventional drug development, the research and development of drugs for orphan indications showed a greater overall return on investment. [1] Orphan drugs are classified as pharmaceutical products aimed at rare diseases or disorders, which in the US means a potential market of less than 200,000 patients. In 1983, the US government passed the financially incentivizing initiative, the ‘Orphan Drug Act of 1983’. Additional markets have emerged since 2000 with the adoption of similar acts in EU and Japan. Drug developers targeting orphan indications have the additional benefits of 7 years of market exclusivity from ‘same drug’ recombinant products (baring clinical superiority), a 50 % tax credit on R&D cost, special grants for phase I – III clinical trial, and user fees waived on revenues <$50 million. These incentives have allowed the development of therapeutics with a limited market financially feasible and as we will see, actually provide a stronger return on investment (ROI) than non-orphan drugs.

According to the new report, worldwide markets for orphan drugs are set to grow from $83 billion in 2012 to $127 billion in 2018 at a compound annual growth return (CAGR) of 7.4 % as compared to 3.7 % for the overall prescription drug market. The financial incentives and expanding market make a strong case for investment in orphan indications; however, the true value to big pharma is derived from the smaller required patient size for approval. Phase III drug development costs can be cut in half or more with an average of 43 % reduced patient size. These results translate into big pharma achieving a 1.7 times greater ROI compared to non-orphan drugs.

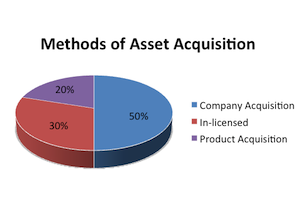

So what is the end result for early stage life science investors? Companies such as Eli Lilly, Roche, and Biogen Idec are acquiring more orphan drug development companies. Of the top 10 orphan R&D products (by NPV) acquired externally, 50% have been the result of company acquisitions, 30% have been in-licensed, and 20% product acquisitions. This is good news for institutional investors looking to exit their investments and foundations looking to advance promising new therapeutics into later stage clinical trials.

So what is the end result for early stage life science investors? Companies such as Eli Lilly, Roche, and Biogen Idec are acquiring more orphan drug development companies. Of the top 10 orphan R&D products (by NPV) acquired externally, 50% have been the result of company acquisitions, 30% have been in-licensed, and 20% product acquisitions. This is good news for institutional investors looking to exit their investments and foundations looking to advance promising new therapeutics into later stage clinical trials.

Beyond the financial incentives for investors and life science companies, this push toward fostering development of previously underdeveloped diseases is benefiting patient groups who previously had scarce treatment options. Take the Cambridge, MA based Aegerion Pharmaceuticals, which is developing the orphan drug lomitapide for patients suffering from a rare form of familial hypercholesterolemia that causes cholesterol levels to soar, followed by almost certain death from heart disease by age 30. The success of the ‘Orphan Drug Act’ leads us to wonder if the poor market performance of other necessary indications will result in similar legislation and resulting financial opportunities. Will we be seeing an ‘Antibacterial Development Initiative Act’ in the future? We’ll keep you posted.

[1] “EvaluatePharma Orphan Drug Report 2013.” EvaluatePharma, n.d. Web. 24 Apr. 2013.