By Shaoyu Chang, MD, MPH, Senior Research Analyst, LSN

The global diagnostics market continues to show robust growth, fueled by aging populations and rising awareness of the value of preventive care. In our recent series of articles, we’ve explored the therapeutic space for cardiovascular diseases, neurology, and oncology. This week, we dive into the diagnostics innovation and investor landscape.

The global diagnostics market continues to show robust growth, fueled by aging populations and rising awareness of the value of preventive care. In our recent series of articles, we’ve explored the therapeutic space for cardiovascular diseases, neurology, and oncology. This week, we dive into the diagnostics innovation and investor landscape.

Two major categories stand out in this space: diagnostic imaging devices and in vitro diagnostics (IVD). Diagnostic imaging devices claimed a global market of US$25.7 billion in 2013, with an estimated annual growth rate of 5.7% for the coming six years.[i] More impressively, IVD claimed a US$47.3 billion global market in 2013, with an annual estimated growth rate of 7.3%.[ii]

Practitioners use a variety of diagnostic imaging technologies, such as X-rays, CT scans, MRIs, PET scans, and ultrasounds, to rapidly determine a medical issue with minimal discomfort for patients. A wide spectrum of IVD technologies, such as point-of-care tests, molecular diagnostics, and hematology tests, can be used to detect or monitor various disease indications in both healthcare and home-care settings.

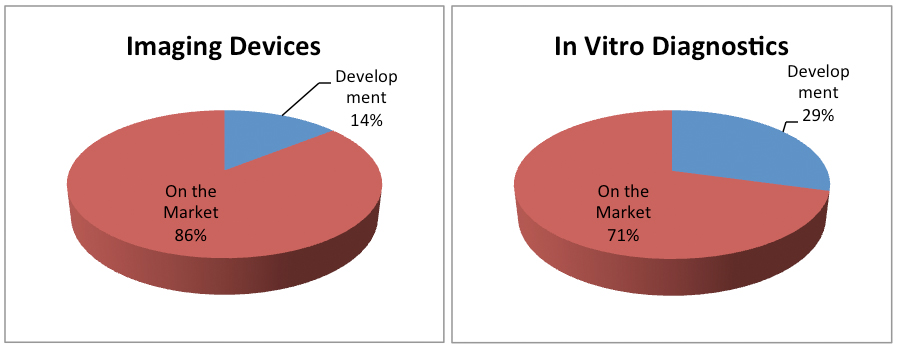

The LSN company database is currently tracking more than 2,500 diagnostic assets globally. As shown in Figure 1, 86% of the imaging assets that we track are approved and on the market. These mature technologies are dominating the imaging market, so innovators are exploring new territories, such as portable and handheld imaging devices and cloud-based digital systems to process, store, and transfer medical images. By contrast, IVD shows more innovation thanks to the past decade’s advances in biology, genomics, and biomarkers for various disease areas.

Figure 1

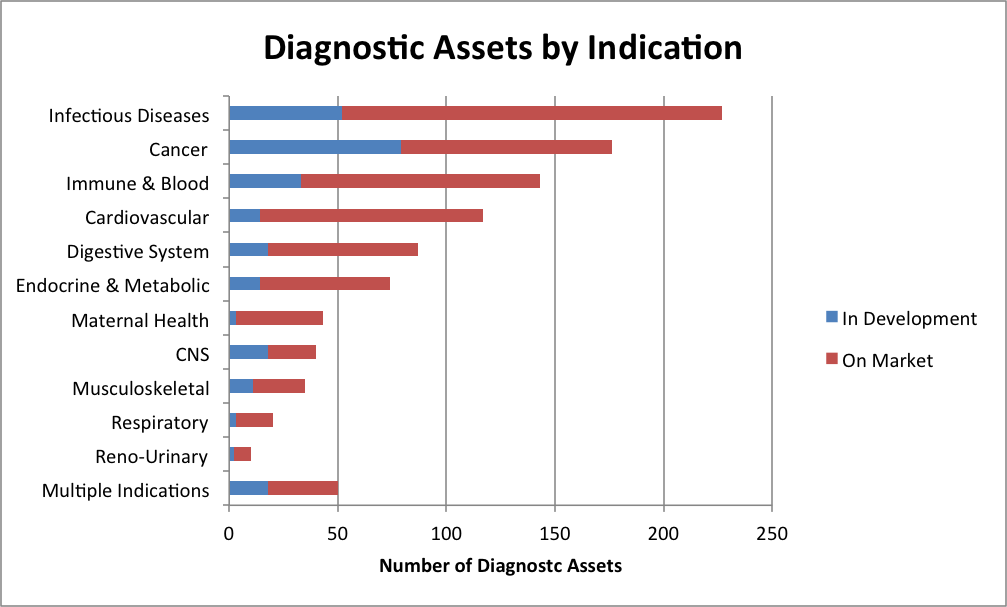

Diagnosing infectious diseases, such as hepatitis, respiratory infections, HIV, and food-borne illnesses, has created a strong demand for diagnostic tools, which is clearly reflected by the data gathered by LSN’s research team and shown in Figure 2. Recent scientific and technical advances are bringing exciting innovations to this field. Examples include microbiome analytics and point-of-care tests that have a wide variety of applications in healthcare institutions and consumer self-care and low-resource settings.

Cancer accounts for the greatest number of assets in development. Cancer diagnostics innovation is partially fueled by personalized medicine and by companion diagnostics that use novel biomarkers to detect traces of tumor cells and differentiate cancer genotypes.

Neurology is a space with a significant amount of product development underway, led by R&D efforts in Alzheimer’s disease and brain imaging technology. Maternal health and cardiovascular diseases have less innovation. Although these areas may present opportunities for innovative companies, they will face a market saturated by well-established products.

Figure 2

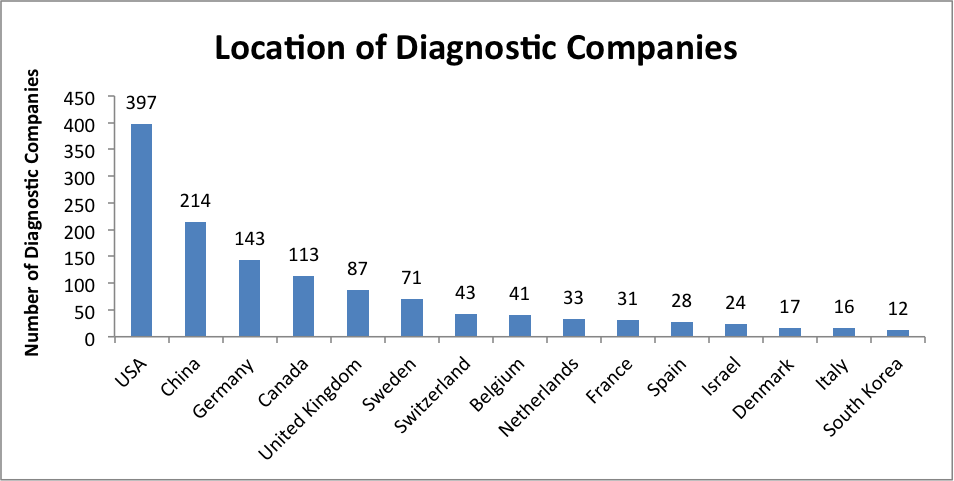

As shown in Figure 3, the U.S. leads other counties in terms of the number of diagnostic companies. Although Western European countries play significant roles in diagnostics, China claims a strong second place with a robust diagnostic industry. As discussed in a previous article, an increasing number of large diagnostic companies in established economies are seeking to penetrate emerging markets though M&A activity. The global diagnostic landscape is changing rapidly, and it is fascinating to watch this space evolves.

Figure 3

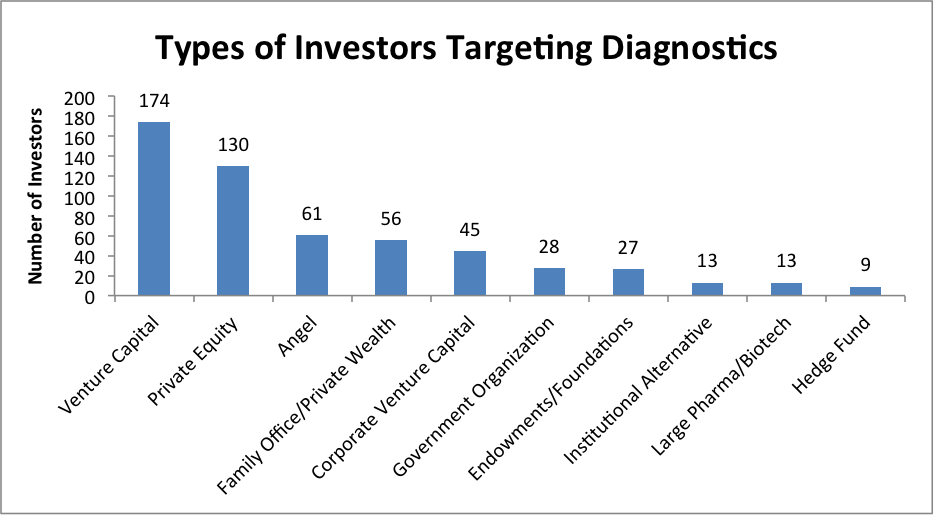

Let’s take a look at the investors in this space. LSN analysts have interviewed more than 500 investors who are interested in imaging and diagnostic devices. As shown in Figure 4, many traditional investors, including venture capitalists, private equity firms, and angel groups, find diagnostic devices attractive because of their short regulatory pathway to commercialization. Pharmaceutical corporate venture capital funds are looking for diagnostic assets to diversify their portfolios. Interestingly, several large corporations in industries other than life science, such as telecommunications and industrial supplies, are also considering using diagnostics and analytics as an entry point to the healthcare arena.

Figure 4

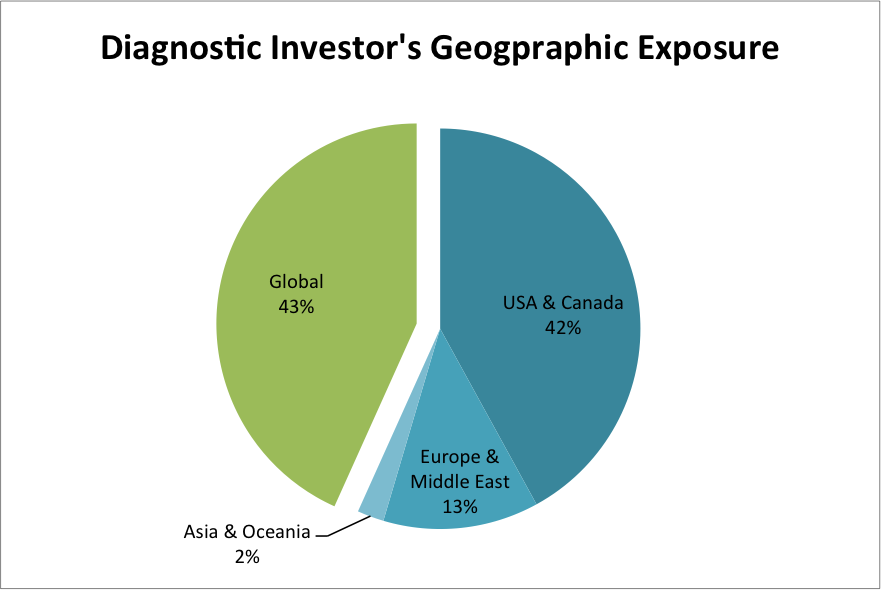

Contrary to the common notion that most investors are regional and only invest in nearby assets, globalization is occurring in the diagnostics investment space, as shown in Figure 5.

Figure 5

Global investors—investors who are active in two or more regions—are leveraging their expertise and extensive network to identify and develop new assets in emerging markets. In addition to raising capital, companies that partner with global investors can sometimes receive assistance navigating regulatory systems and gain a stepping stone into unknown markets. Cross-regional cooperation has become increasingly commonplace, and we expect the trend to continue in the future.

[i] Medical Imaging Systems Market (Portable, Handheld X-Ray Devices, CT, Ultrasound, Open and Closed MRI and Nuclear Imaging, Analog, DR, CR, 4D and 5D, Low Slice, Medium Slice, High Slice Scanners) Analysis and Segment Forecasts to 2020, Grand View Research, June 2014.

[ii] Analysis of the Global In Vitro Diagnostics Market, ReportLinker, July 2014.

Leave a comment