By Shaoyu Chang, MD, MPH, Senior Research Analyst, LSN

Mimi Liu, Research Analyst, LSN

As the world’s second largest pharmaceutical market with an estimated annual growth rate of 10%–13% through 2018[1], China continues to attract growth-seeking life science companies and investors from across the globe. What are the opportunities and challenges in entering in this market? This article provides an in-depth view by dissecting information gleaned from LSN’s company platform and the interviews we have conducted with investors based in Greater China.

As the world’s second largest pharmaceutical market with an estimated annual growth rate of 10%–13% through 2018[1], China continues to attract growth-seeking life science companies and investors from across the globe. What are the opportunities and challenges in entering in this market? This article provides an in-depth view by dissecting information gleaned from LSN’s company platform and the interviews we have conducted with investors based in Greater China.

The growth of China’s pharmaceutical market is driven by a large and aging population, increased access to healthcare, and nationwide policy reform. Over the past five years, the generic drug market has been growing steadily, while branded drugs have gained greater protection, due to the improvement of regulations and laws by the China Food and Drug Administration. Market demand has shifted from antibiotics to specialized drugs, with many therapeutics companies starting to focus on oncology, cardiovascular conditions, blood diseases, and supplements.[2]

We examined a sample of 553 innovative companies located in Mainland China, Taiwan, and Hong Kong that are developing biopharmaceutical assets from the preclinical through phase 2 trial phases (see Figure 1). Neoplasm and “lifestyle diseases,” including metabolic and cardiovascular diseases, have attracted the most number of biopharmaceutical innovators. These therapeutic indications are of high demand domestically with the potential of expansion into overseas markets. A significant number of innovative companies are working on infectious diseases that are endemic to the region, such as hepatitis, tuberculosis, and HIV. However, there seem to be fewer innovations in diseases of the nervous, digestive, and respiratory systems, despite their high health burden.

Figure 1 | Source: LSN Company Platform, Data as of April 15, 2015

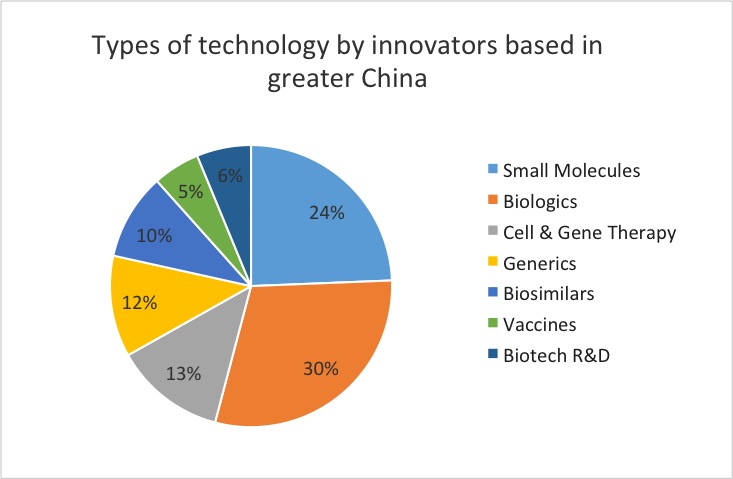

The development of China’s biotechnology sector is fueled by R&D centers set up by big pharmaceutical companies as well as the recruitment of Chinese expatriate talents, or “Haigui.” State-backed bioclusters are emerging in Beijing, Shanghai, Jiangsu, Shenzhen, Hong Kong, and Taiwan. Over half of the innovators in the region are developing therapeutics, including small molecules, antibodies, proteins, peptides, and nucleic acid drugs, as shown in Figure 2. There is also a significant interest in generics and biosimilars that addresses the strong demand for high-quality, low-cost products for the vast population.

Figure 2 | Source: LSN Company Platform, Data as of April 15, 2015

Medical device sales in China reached US$32 billion in 2013, making the country the second-largest market in the world[3]. Domestic manufacturers traditionally dominate the hospital equipment market, including medical carts, operation room and ICU equipment, and autoclave sterilizers. Devices for surgical, orthopedic, and dental use are also an arena saturated with locally based companies. According to BMI Espicom, China still has a high demand for imports, especially in the diagnostic imaging sector[4]. With the rise of cross-border partnership with international device manufacturers such as Johnson & Johnson, original equipment manufacturing (OEM) and original design manufacturing (ODM) have become important business units for medical technology companies in the region.

“Medical technology has been part of China’s national development strategy with increasing importance,” said Dr. Fan Yubo, president of the Chinese Society of Biomedical Engineering, at a recent medical device industry summit. “China’s upcoming 13th Five-Year Plan will focus on digitalized diagnostics, tissue repair and regenerative materials, molecular diagnostic tools and reagents, artificial organs and life support equipment, and health monitoring devices.”[5]

Let us take a look at the life science investment landscape in the region. To date, the LSN research team has spoken to over 50 life science investors who are based in Mainland China, Hong Kong, and Taiwan. While large pharmaceutical companies and venture capital funds are traditionally major players in this field, we have seen a growing trend of private equity funds, state-backed funds, and family offices showing an interest in life science investments, as shown in Figure 3.

Figure 3 | Source: LSN Investor Platform, Data as of April 15, 2015

We found that the investors who exclusively focus on China or Asia are typically interested in companies in clinical phase 2 or later of their development pipeline. On the other hand, about two-thirds of Greater China-based investors would like to look at new opportunities across the globe, with a specific focus on North America and Western Europe. These investors are generally stage agnostic, and many have a mandate to introduce cutting-edge technology back to the Chinese market.

During our conversations with those investors, the majority showed high interest in diabetes, cardiovascular, cancer, respiratory, digestive system, and nutrition fields, which are of great significance to the region. For example, China bears the highest burden of diabetics in the world, with an estimated 100 million people living with the disease[6]. One in five adults in China suffers from cardiovascular disease, which accounts for 40% of all deaths[7]. Moreover, the incidence of lung cancer in China has grown exponentially since the 1970s, due to smoking and air pollution. The disease is now the number-one cancer killer in the country, with over 487,000 new victims in 2010[8].

China represents immense opportunities for development of novel therapeutics and medical devices due to factors such as rapid market growth, the concentration of an educated workforce, and improving intellectual property protection and regulatory environment. In the medtech sector, state-led initiatives have identified high-end digitalized diagnostics, imaging devices, molecular diagnostic tools, and health monitoring devices as key strategic fields of development. Disease areas of the nervous, digestive, and respiratory systems present with high disease burden and relatively fewer innovations. Innovative biotech and medtech entrepreneurs should be able to find plenty of potential investors, as well as cross-border cooperation in R&D and manufacturing.

[1] IMS Institute. “Global Outlook for Medicine Through 2018”. Page 20. Web. 2014. Accessed from http://static.correofarmaceutico.com/docs/2014/12/01/informe_ims.pdf

[2] Feng Chao. “Future Trends in China’s Pharmaceutical Industry and Case Studies” (in Chinese). Web. 2013. Accessed from http://blog.sina.com.cn/s/blog_5d30c7960101pqxk.html

[3] Steven Elsinga. “Market Overview: The Medical Device Industry in China”. China Briefing. 2014. Accessed from http://www.china-briefing.com/news/2014/12/03/market-overview-medical-devices-china.html

[4] Jamie Hartford. “The Medical Device Market in China”. Medical Device and Diagnostic Industry Website. 2013. Accessed from http://www.mddionline.com/article/medical-device-market-china

[5] Chinese Society of Biomedical Engineering. “Fan Yubo: Initial View on the Medical Device Strategies in the Thirteenth Five-Year Plan”. Chinese Society of Biomedical Engineering Website. 2015. Accessed from http://www.csbme.org/csbme/ch/showNewsDetail.asp?nsId=231

[6] Veronica Hackethal. “Diabetes Is a Major Public-Health Crisis in China”. Medscape. 2014.

[7] Editorial. “Cardiovascular Disease in China:Why Should We Care.” Journal of Asian Health. 2015. Accessed from http://journalofasianhealth.com/cardiovascular-disease-in-china-why-should-we-care/

[8] Chen W, Zheng R, Zeng H, and Zhang S. “The Epidemiology of Lung Cancer in China”. Journal of Cancer Biology and Research. 2014. Accessed from http://www.jscimedcentral.com/CancerBiology/cancerbiology-spid-lung-cancer-china-1043.pdf

Leave a comment