By Dennis Ford, Founder & CEO, LSN

Executing a successful fundraising campaign in the life sciences space requires organization, professionalism, determination, a great technology, and an outstanding team. LSN has worked with hundreds of companies in this capacity—companies that are at all stages of development, in regions around the world, and pursuing various types of technology. We’ve been watching as the latest process for fundraising has surfaced, and I wanted to share what we see as the ten steps.

Executing a successful fundraising campaign in the life sciences space requires organization, professionalism, determination, a great technology, and an outstanding team. LSN has worked with hundreds of companies in this capacity—companies that are at all stages of development, in regions around the world, and pursuing various types of technology. We’ve been watching as the latest process for fundraising has surfaced, and I wanted to share what we see as the ten steps.

1. Company Assessment

The first step in your fundraising campaign should be a general assessment of your intentions and your company. The questions to be answered include: How much capital do you plan to raise? What will the funding be used for? What are the R&D milestones? Elucidate the risks and how you plan to mitigate them. And calculate your company’s current valuation. Painting a rosy picture is the kiss of death. Being up front, candid, and honest validates your credibility.

Most important, determine how quickly you need the capital. Note that it takes 9 to 18 months to get funded.

Raising capital is resource intensive, which raises another question: Who is going to take on this job? Recently during a three-month campaign, LSN staff identified 360 global-investor targets, sent out 600 emails, and made 400 phone calls in order to get 25 meetings. Are you or your designated point person the right one to handle this job?

When answering these and the many other questions that come up during a company assessment, it is best to consult with several trusted and reputable sources to fully assess your opportunity and determine how best to position yourself.

2. Marketing Collateral

When you have a firm grasp on how you are planning to position yourself to potential investors and who will be reaching out, you need to develop marketing materials that clearly and succinctly describe your opportunity. Essential materials include a logo, tagline, elevator pitch, executive summary, PowerPoint presentation, and a website.

These materials will be your face to the investment community, and as such, they should be drafted with careful consideration. It is crucial that you do not drown potential investors in reams of data and articles from scientific journals supporting your science. Don’t try and prove the market for your product; investors already understand the market-size element. Tell the story of the technology; tell the story of how the management team found each other and bonded; make the story simple and easy to grasp.

When crafting your materials, remember that investors are busy. Some have told LSN that they receive 500 to 800 solicitations a week, so you have to quickly and adroitly communicate your value. Initially, you may get five to ten seconds of an investor’s time on your home page. The purpose of your marketing materials is to pique an investor’s interest enough that he or she agrees to set up a meeting to learn more, not to close a deal.

Interested investors will thoroughly review all your data and journals at the due diligence stage, but they won’t invest time up front to review your materials if your opportunity isn’t presented in a way that clearly demonstrates its value to them.

3. Global Target List

Make no mistake about it: fundraising is a numbers game. Only using personal networks and staying regional is a waste of time. You need to find as many investors as you can who are a fit for your sector and the stage of your company. The only way to do this is to aggregate a list of global investors who are a potential fit for your firm and canvass them through email and phone.

Identifying potential investors is no small task. With investors moving in and out of the space, and with many investors maintaining a very low profile, this step can take a considerable amount of time to do well.

Here at LSN, we identify investors using a number of methods, including previous financing rounds, conference attendee lists, news feeds, and networking events. When looking for potential investors, you need to consider your company’s stage of development, technology type, indication area, region, and the amount of capital you are looking to raise.

You should be looking for investors who have historically invested in companies similar to yours or for partners that have experience in your field of medicine. When looking for investors, you will more than likely come across those who tend to look at later stage opportunities. These investors should absolutely be included in your list. Although they aren’t an appropriate investor for your company at this stage, by beginning a dialogue with them now, you can keep them abreast of what you are doing, which will make securing later-stage financing much more efficient.

Using the LSN investor platform, our business development folks can generally identify from 250 to 400 investors across ten categories for a given opportunity based on fit. We will canvass them, and those who show an interest are the ones we go after and concentrate on. These targeted campaigns uncover investors who are active and looking to fulfill their investment mandates. If we target 400 investors, that group usually gets whittled down to 60 to 80 investors who merit some time. That’s how the numbers game works. In turn, that group of 60 to 80 investors is narrowed down to 20 to 30, then to 10 to 12, and eventually to the 2 or 3 that will invest in the round. All this takes time and focus and leads us to the next part of the process, which is getting the tools in place to handle a list of 400 investor candidates and the associated tasks.

4. Cloud-Based Application

Staying on top of that many contacts can be overwhelming; however, it is made drastically easier through cloud-based applications such as SaleForce.com. Such applications provide a list-management and task-management system. Note that if you’re using a spreadsheet, you have already lost the battle. SalesForce.com ($5.00 a month) can help you store, organize, and classify the data and contact information for all of the investors on your list, as well as allow you to set follow-up dates to better understand who you need to be contacting and when. Other useful pieces of infrastructure to consider include an email-tracking system, such as Constant Contact or iContact, that allows you to see when people are opening and clicking on your emails to determine your hottest targets. These applications are also online-content generators, which you can use to publish articles and other content surrounding your opportunity.

5. Conference List and Outbound Campaign

With your cloud infrastructure in place, you need to organize your road show. You need to determine which investment and partnering conferences are taking place during your campaign and which ones you should be attending. Ideally, you will be able to book conferences across the world to meet with various investors. Additionally, you should be aligning your outreach to try and book meetings with investors who have offices near the conferences you are attending even if they aren’t going to the event. Investors tend to be more responsive if you tell them the brief window of time during which you will be in town, and you should take full advantage of that. A conference-only strategy is a nonstarter. You need to dig in and use every available means to get out of office and in front of investors. I call it the last three feet: when you stick out your hand and introduce yourself, the game is afoot!

6. Campaign Execution

It takes money to make money. One year on the global fundraising trail is going to cost you $80,000 to $100,000. Marketing collateral, website development, road trips, conferences, and regional and global travel—it all adds up. In fact, the latest trend is for investors to demand that 10 to 20% of the funds be set aside for future market development. Budgeting and capital planning is all part of adroit execution. This is where the rubber meets the road. With your materials, infrastructure, and plan in place, you need to physically begin the outreach to potential investors. This should be done through an email-marketing campaign that coincides with a phone-canvasing campaign that is tracked and managed through your cloud infrastructure. You need to focus on taking cold leads off the table and moving forward with the good ones.

7. Scheduling and Logistics

When you get investors interested, you need to act quickly to book meetings. Whether it’s over the phone or the more preferable in-person meeting, you need to get it on the schedule quickly. If it’s an in-person meeting, tackle the logistics equally as quickly. Identify your transportation and accommodations for the trips you will be taking. By working out some of the details of your travel plans during the outreach phase, you have the opportunity to meet with more investors in the regions you will be visiting.

8. Meetings

When attending meetings and conferences, you should bring your A game. You should be prepared to answer all questions investors may pose and take diligent notes on the points they make. It is also important to not hide the risks associated with your investment at this stage. Investors understand that life science investing is inherently high risk, and if they uncover something later in the due diligence phase that you didn’t tell them up front, they may feel their trust was misplaced and the deal could sour. You should view networking at conferences and events as very much a part of your job, you never know who may be able to connect you to who so it is important to always remain professional about what you are doing while managing to shake as many hands as possible.

9. Conference Report and Road Trip Reports

Throughout the various meetings and conferences, you will be getting a lot of different feedback, both positive and negative, from investors. As you continue to move forward, you should be aggregating all of this feedback and periodically be making full reports for colleagues based on what you hear. What are the most common reasons investors decline to meet or move forward? What seems to grab their attention? What are their most common questions? Answers to these questions and others should all be included in the report and should be taken into consideration when you tweak the marketing materials. In fact, if the feedback seems to point strongly in a direction that is different from the one you are currently pursuing, you should consider pivoting your company. This report should be shared throughout your company and, in particular, with your board to keep them up to speed with the fundraising campaign and to demonstrate how the marketplace is viewing the opportunity.

10. Investor Follow-Up

Properly using the cloud infrastructure can make your follow-up process much more efficient. You can set dates for follow-up at any time using the task- and relationship-management software. You should absolutely hold yourself to the dates you set. Moving interested investors deeper into the due diligence stage and keeping later-stage investor abreast of your progress will save you time and increase your odds for success. Also, you need to be constantly parsing and changing your target list to reflect your hottest leads to ensure you spend more time working towards your best targets and do not spend hours trying to contact investors who aren’t interested.

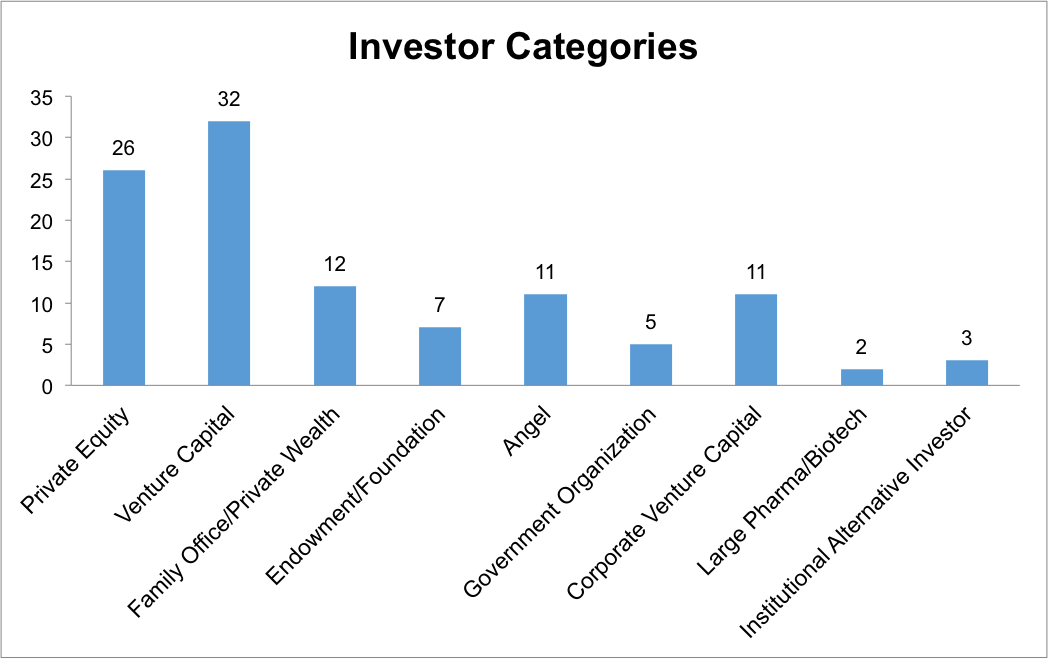

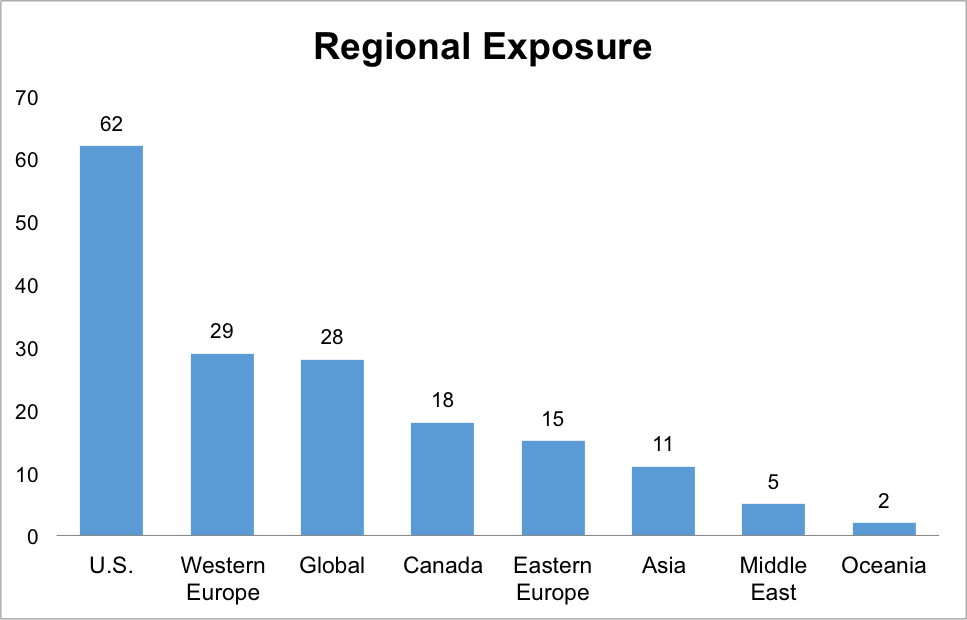

Last week, the LSN research team closed out the first month of the last quarter, tallying and analyzing the investor mandates gathered throughout October. Our researchers spoke with 109 deal-sourcing executives last month. As usual, these investors were highly diverse, hailing from 20 countries and representing 9 investor categories; 12 of the 109 were investors from family offices and private-wealth funds. (See Figure 1.)

Last week, the LSN research team closed out the first month of the last quarter, tallying and analyzing the investor mandates gathered throughout October. Our researchers spoke with 109 deal-sourcing executives last month. As usual, these investors were highly diverse, hailing from 20 countries and representing 9 investor categories; 12 of the 109 were investors from family offices and private-wealth funds. (See Figure 1.)

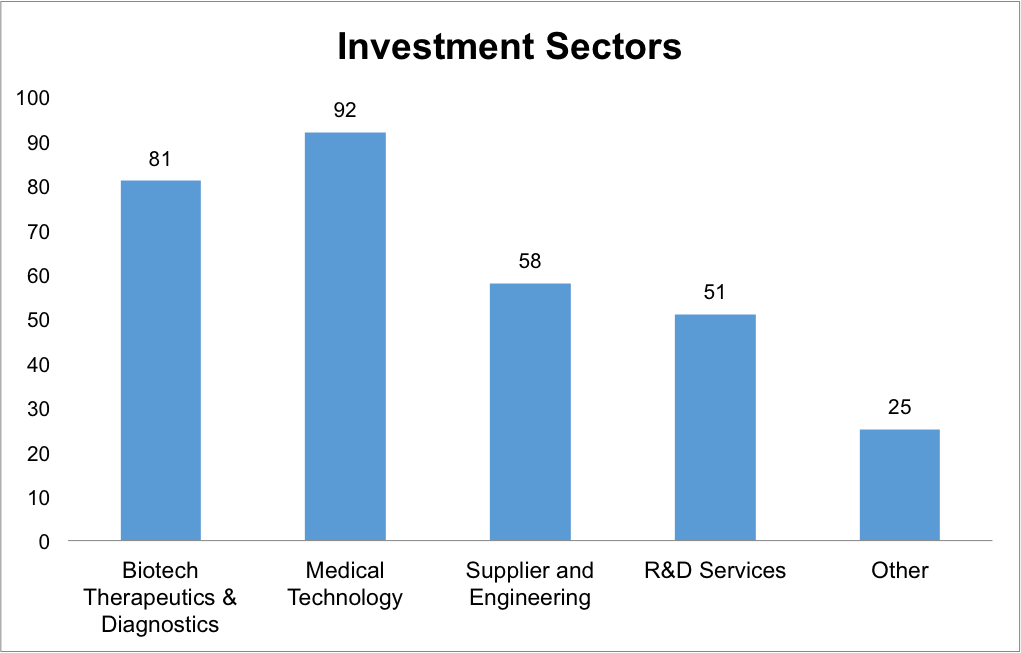

The biotechnology industry is growing in the Asia-Pacific and Latin America regions,

The biotechnology industry is growing in the Asia-Pacific and Latin America regions,![RESI-4-Banner-3x8[5]](https://blog.lifesciencenation.com/wp-content/uploads/2014/10/resi-4-banner-3x85.png?w=490)

{kind=link}