By Michael Quigley, Director of Research, LSN

Several significant factors have been attracting capital to the life science sector over the past two years. An IPO explosion has provided many life science investors with positive exits, and, in turn, they have established new funds to put some of that capital back to work. In addition, new investors have come to the sector as a result of the number of successful IPOs and low interest rates; investors are looking for better returns. These factors led to life science funds raising an estimated $3.5 billion in 2013 alone.[1] Several funds have continued to raise capital this year.

Several significant factors have been attracting capital to the life science sector over the past two years. An IPO explosion has provided many life science investors with positive exits, and, in turn, they have established new funds to put some of that capital back to work. In addition, new investors have come to the sector as a result of the number of successful IPOs and low interest rates; investors are looking for better returns. These factors led to life science funds raising an estimated $3.5 billion in 2013 alone.[1] Several funds have continued to raise capital this year.

This is positive news for fundraising entrepreneurs, and their next step should be to pinpoint the funds that have raised new capital and their investment targets.

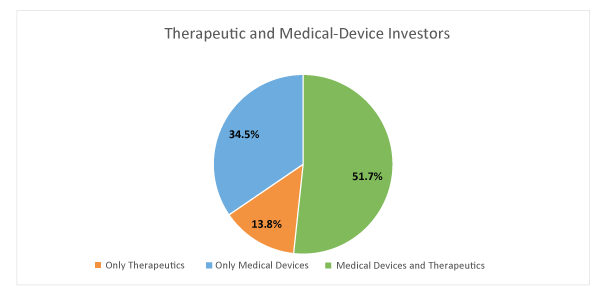

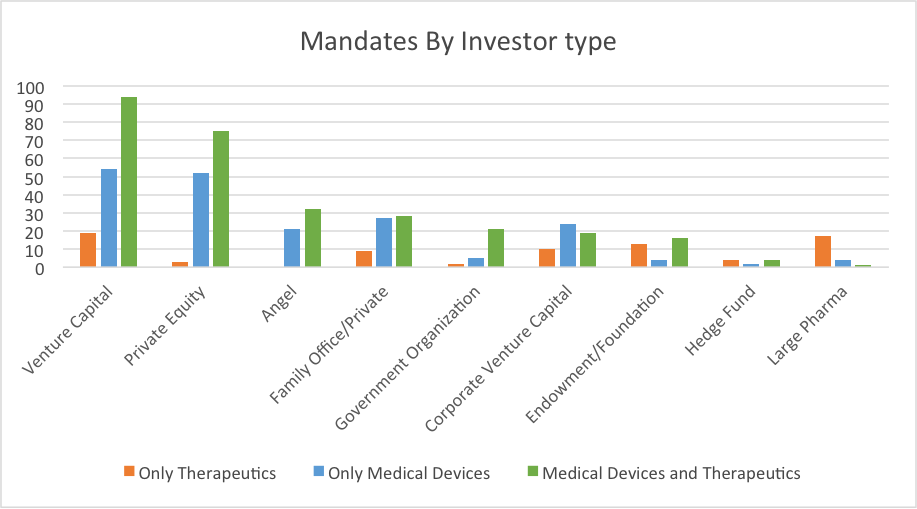

The LSN research team has identified and interviewed more than 100 investors who have raised new capital since 2012. These investors fall in eight categories. (See Figure 1.)

Figure 1

Venture capital and private equity represent the largest number of investors; however, the other investor types represent a significant amount of new capital. Although each of these investor categories have various motivations for investing in the space—for example, financial, philanthropic, or strategic—it is promising to see so many groups with new capital to allocate to the space.

Also worth noting are the regions where these investors are based. The investors we identified are based in 20 countries in North America, Europe, and Asia, and Oceania. (See Figure 2.)

Figure 2

This distribution of investors with new capital reflects the IPO environment in these regions. The U.S. and therefore North America has had the highest number of IPOs, followed by Europe and Asia and Oceania. More important than where the investors are based, however, is where they are looking to allocate. Of the investors we spoke with, more than 50% are looking to invest across continents or globally. Previous articles in this newsletter have discussed the globalization of investment in the life science sector; this trend is validated by the current interests of funds and investors.

It would appear that the time is now for a start-up to execute a fundraising campaign if it has the data and team to support it. Not only is there capital to be had, but early on in a funds lifecycle, investors often consider research and technologies at earlier stages of development as the investors have the time and capital on hand to support them.

[1] Life Sci VC, “Perspectives on VC-Back Biotech: Looking Backward & Forward,” 2013 (http://lifescivc.com/2014/01/perspectives-on-biotech-looking-backward-forward/).

The role of corporate venture capital (CVC) continued its remarkable expansion in 2014. In the second quarter, CVC funding accounted for 29% of total venture capital funding. In the healthcare sector alone, CVC funding soared to a five-quarter high of $1.4 billion, up 200% from the previous quarter.

The role of corporate venture capital (CVC) continued its remarkable expansion in 2014. In the second quarter, CVC funding accounted for 29% of total venture capital funding. In the healthcare sector alone, CVC funding soared to a five-quarter high of $1.4 billion, up 200% from the previous quarter.

As LSN prepares to bring the next Redefining Early Stage Investments Conference to San Francisco, we are proud to announce that emerging biotech and medical device companies

As LSN prepares to bring the next Redefining Early Stage Investments Conference to San Francisco, we are proud to announce that emerging biotech and medical device companies

{kind=link}