By Lucy Parkinson, Senior Research Manager, LSN

In last week’s newsletter, we presented an overview of innovation and investment in the cardiovascular space. This week, we continue this series, analyzing LSN data on the neurology sector. Investors often tell us that neurology is a challenging space, particularly when it comes to evaluating early stage opportunities; some investors feel that it’s harder to assess animal data or prototype studies in this space than it is in many others. Here, we take a look at the competitive landscape for neurology and the investors.

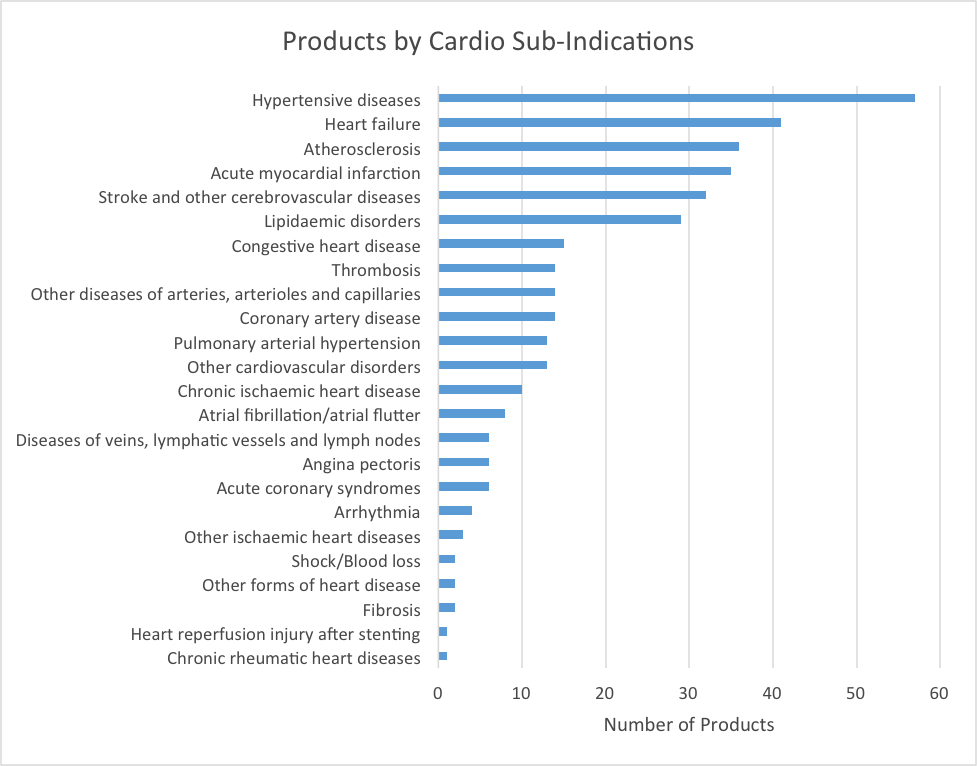

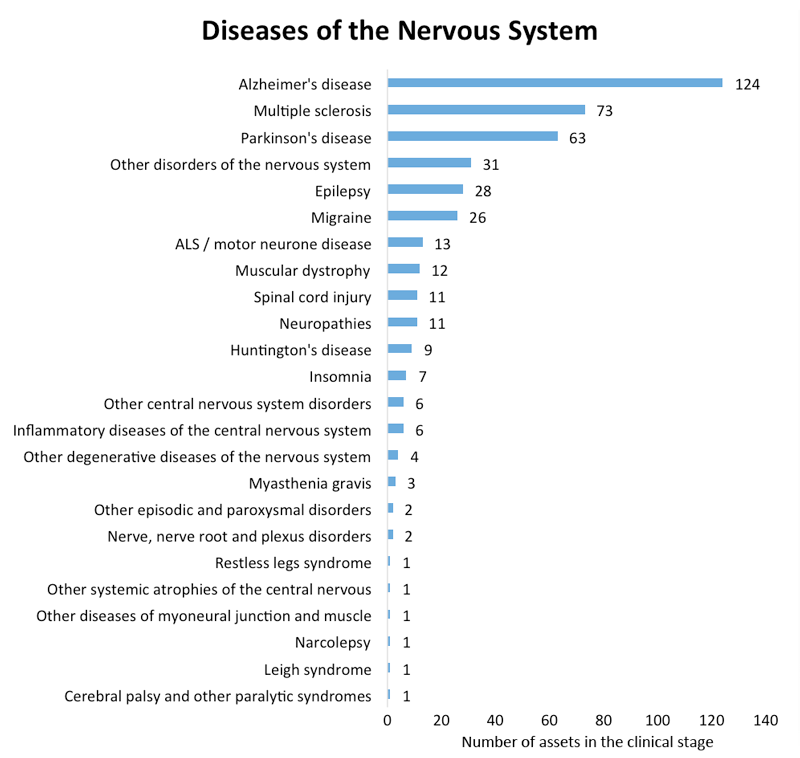

LSN tracks therapeutic assets for two areas of neurology: diseases of the nervous system and mental and behavioral disorders. The former is a far more robust area of innovation at present, with 646 assets in clinical trials. We have been able to determine the specific disease areas that 437 assets are targeting. (See Figure 1.)

Figure 1

For many severe neurological disorders, there is tremendous competition among treatments at present; more than one hundred Alzheimer’s cures are presently in clinical trials, as are dozens of potential treatments for Parkinson’s disease, multiple sclerosis, and epilepsy. However, the pipeline is limited or dry for many rare neurological disorders. Leigh syndrome, a severe pediatric disorder, has only one asset in the clinical stage. For some other indications that we track, including Charcot-Marie-Tooth disease and Steinert disease, no drugs are currently in clinical trials. Potential treatments for these rare diseases could qualify for an orphan drug designation, so an early stage investment could yield not only a life-changing result for thousands of patients but also an opportunity for an investor to benefit from limited competition and a long period of exclusivity after the treatment has received approval.

Less innovation is taking place to address mental and behavioral disorders; only 164 therapeutic assets are in clinical trials. We have been able to determine the disorders that 144 assets are targeting. (See Figure 2.)

Figure 2

There are fewer medtech neurology products in the development stage because they have a shorter development cycle. We have identified and categorized 119 such products that are aiming to treat neurological, psychiatric, and spinal disorders, and in 100 cases we were able to identify the type of device being developed. (See Figure 3.)

Figure 3

Some areas of innovation are seeing markedly more new products than others; electromechanical devices (such as neurostimulation devices) form a crowded competitive field, as do various forms of implantable devices, many of which are targeting the spinal care market. There is also a wide variety of neurological diagnostic and imaging technologies in development. By contrast, few inventors are developing technical aids for patients suffering from neurological disabilities.

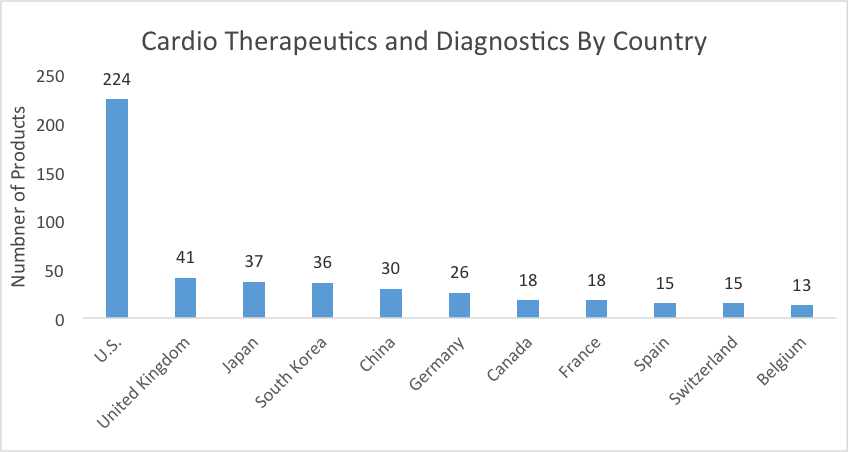

Neurology innovation is occurring worldwide. The U.S. has the largest number of neurology companies in both the biotech and medtech sectors, while in other respects the distribution of biotech companies is quite different from the distribution of medtech companies. (See Figures 4 and 5.)

Figure 4

Figure 5

The UK, Japan, and France are among the top five countries that have the highest number of biotech neurology companies, but these countries fall behind Germany, Spain, and Switzerland when counting the number of medtech neurology companies in each country. Canada is a leader in both sectors.

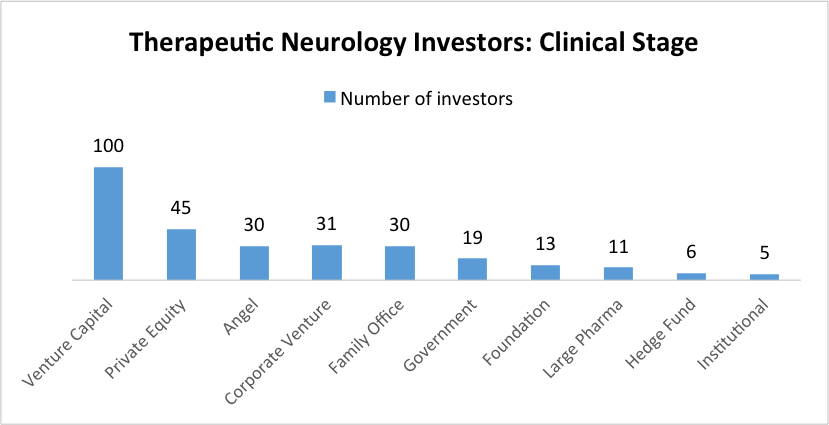

Now, let’s take a look at the investors interested in the neurology space. LSN has spoken with the investment staff at 290 organizations that are open to investing in therapeutics in the clinical stage. (See Figure 6.) We also spoke with 386 organizations that are interested in neurotech devices that are in the development or clinical stages.

Figure 6

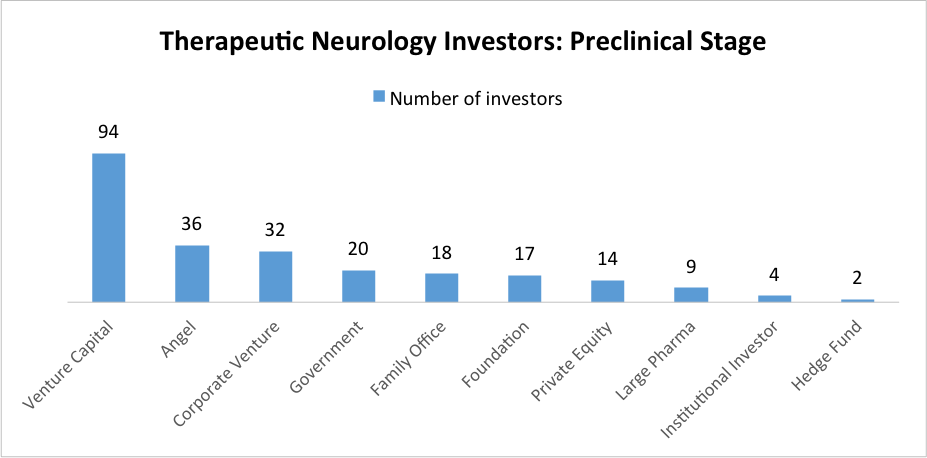

It’s interesting to see that if we look at investors interested in neurology therapeutics in the preclinical stage, we find a different pattern. (See Figure 7.)

Figure 7

Venture capital is the largest category of investors in both cases. But at the preclinical stage, angel groups, corporate venture capital funds, and foundations—all of which may be more prepared to take on risky neurology assets in return for the possibility of developing a new cure in the future—play a more prominent role.

On the medtech side, private equity firms show more willingness to get involved in products that have yet to achieve approval. (See Figure 8.) In many cases, these firms are interested in providing funds to companies that are close to receiving approval for their products and need capital for commercialization.

Figure 8

Where are these investors willing to allocate their capital? While many neurology investors are focused on the U.S. and Western Europe, a large number are looking globally, particularly those interested in the biotech sector.

Figure 9

In addition to the multitude of global neurology investors, LSN researchers have spoken with investors who are interested in investing regionally around the world.

Both global and local capital provide possibilities for companies in the neurology space. No matter where your company is based, we’ve found investors who would like to see what you’re working on.

Here at LSN, we’re getting ready to go home for Thanksgiving. But first, we’d like to thank all our readers, supporters and friends across the global life science industry. We wouldn’t be here without you.

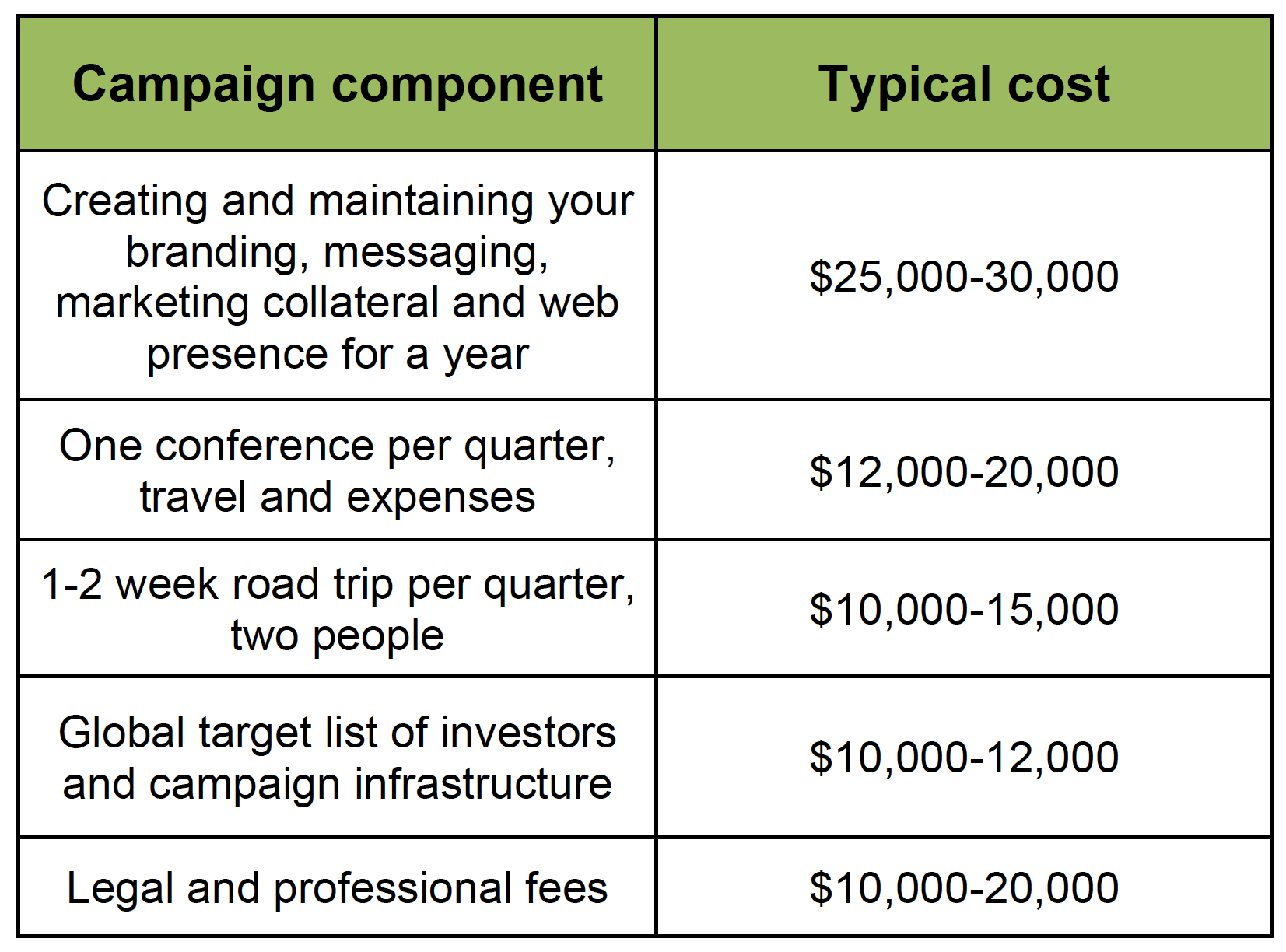

Here at LSN, we’re getting ready to go home for Thanksgiving. But first, we’d like to thank all our readers, supporters and friends across the global life science industry. We wouldn’t be here without you. Coming from a scientific background, I thought I knew well enough about using slides and making presentations, whether in laboratory journal clubs or at hundred-attendee conferences. However, as I start to help fellow scientists on their fundraising campaigns, it has become apparent to me that academia and business speak very different languages.

Coming from a scientific background, I thought I knew well enough about using slides and making presentations, whether in laboratory journal clubs or at hundred-attendee conferences. However, as I start to help fellow scientists on their fundraising campaigns, it has become apparent to me that academia and business speak very different languages.

RESI has always aimed to bring a diverse pool of investors together to meet life science entrepreneurs, and at past events, our Family Office panels have often

RESI has always aimed to bring a diverse pool of investors together to meet life science entrepreneurs, and at past events, our Family Office panels have often