By Michael Quigley, Director of Research, LSN

For nearly 3 years the LSN research team has been identifying, profiling and interviewing early stage life science investors from around the globe. Throughout this time we have developed and honed a process for the identification and validation of investors in order to understand and qualify their investment interests. I recently held a “Researching Global Investors” workshop at our RESI 4 conference to shed light onto this process and share the tools and resources that we use, so that the entrepreneurs in the audience can take advantage of them as well. This article mirrors the workshop to further spread the message to our readership.

Tools for Identification:

Understanding where to look to find potential investors can seem like a daunting task given the vastness of the internet; however, by understanding the tools at your disposal, you can dramatically increase the effectiveness and efficiency of your research. Google search is often underutilized by those unaware of its capabilities. The chart below shows some basic “boolean” operators that can dramatically increase the precision of your searches.

These functions can be entered into the Google’s search bar to make your searches are more targeted and fruitful. For example, by entering (intitle:biotech AND “Invest” AND “Early Stage” –public) into Google, you can search the web for sites and articles that have “biotech” in the title, include the terms “early stage” and “Invest”, and do not include the word “public”. Boolean functions should be utilized in whatever way makes the most sense for your campaign; this could include looking for terms surrounding your indication, stage of development, geographic exposure, or other factors that define your opportunity. By executing a number these searches and diving through a few pages of results you are sure to come up with a size-able number of potential investors.

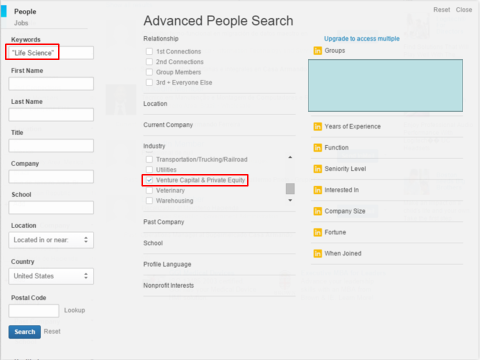

Another often underutilized tool is LinkedIn. Similar to Google, LinkedIn search is also compatible with boolean operators, so using these in the search can again improve effectiveness. LinkedIn also offers an Advanced People Search feature that includes keywords, company name, industry and location among other details, as seen below. An additional benefit of using LinkedIn is that investors and others who are active LinkedIn users with complete profiles are often more open to being approached with opportunities. As LinkedIn is a professional networking site, these individuals tend to be more open to new contacts, and may even be actively looking to expanding their networks and uncover new opportunities.

Additional sources for new investor leads include life science investor conferences, and the websites of companies similar to your own. Investor conferences often list attending investors on their webpages, so even if you cannot attend an event, these can be great sources for identifying active investors. Much like investor leads found on LinkedIn, investors found on conference lists tend to be actively looking for new opportunities; this is generally their motivation for attending the conference. Now, visiting similar companies’ websites to find investors may seem like a stretch; however, many companies list their investors on their website, and if they are in a similar space and stage as your opportunity it is highly likely that those investors are a great fit. Also, many companies list their board of directors on their webpage as well; oftentimes members of the board are investors, as investors generally look to take a board seat following investment.

Validation:

Once you have identified a number of potential investors using the aforementioned methods, you must validate that these investors are a good fit for you opportunity. There are several variables you should consider, the first of which is determining if the investor is currently allocating. When attempting to determine if an investor is currently allocating you want to look for the most recent new investments that investor has made. These can be found either on the webpage of the investor or through using Google searches to find press releases or media articles relating to the investor’s recent deals. The more recently the investor has made a new investment, the more likely that they are still currently investing. Another means of identifying investor activity is to look at the most recent fund vintage. Funds generally have a 10 year lifecycle from closing until they need to return capital to their limited partners. As such, if your company requires 3-5 years to reach a potential exit, you will want to identify funds that have closed no more than 5 years ago. Funds generally reserve capital for follow-on investments, so it is highly likely that funds greater than 5 years old are no longer making new investments at all. They are instead reserving the fund’s remaining capital to support current portfolio companies.

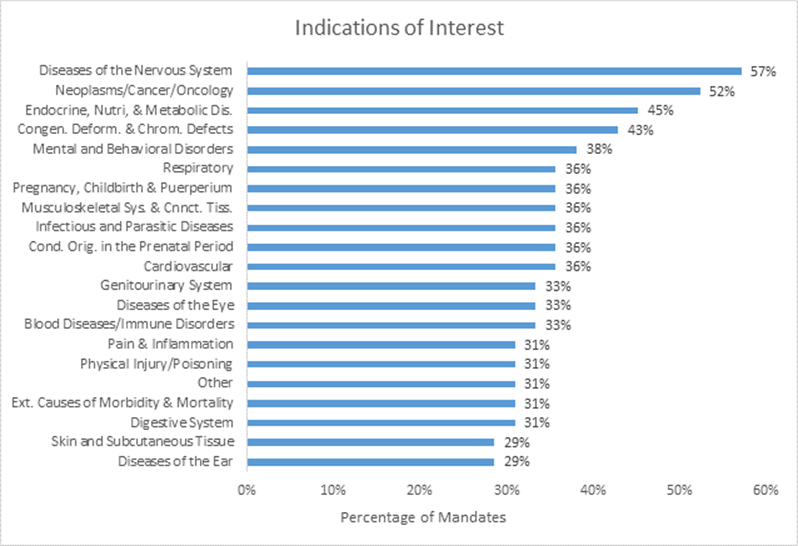

Other variables that require validation include the investor’s preferred stage of development, industry sector, indication areas and geography. While many investors also list these criteria on their webpage, others are more reticent. For investors who do not list their criteria on their web page, the best place to look to find it would be in the firm’s previous investments. Have they invested in medical devices, or in therapeutics? Do they only invest locally, or will they look at opportunities globally? Do they invest in series A rounds, or are they only investing in later stage companies? Many of these questions can be answered by taking a look at previous investments the investor has made. Information on these previous investments is often available in press releases that can be found through searching the web.

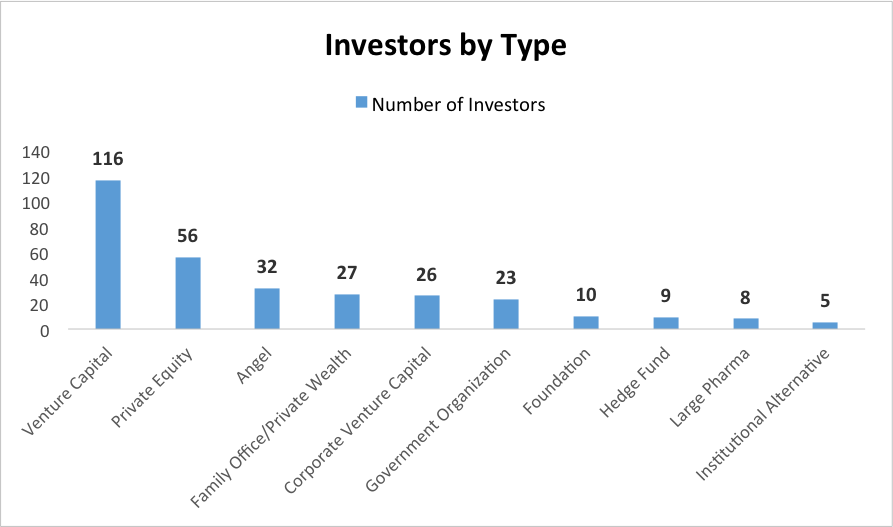

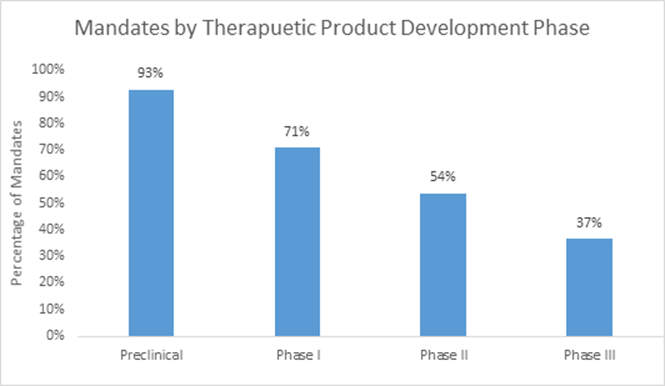

The type of investor you are researching can also be a telling sign of the stage of investment they are looking for. The chart below provides a visual representation of the different stages of therapeutic development that different classes of investors are generally interested in.

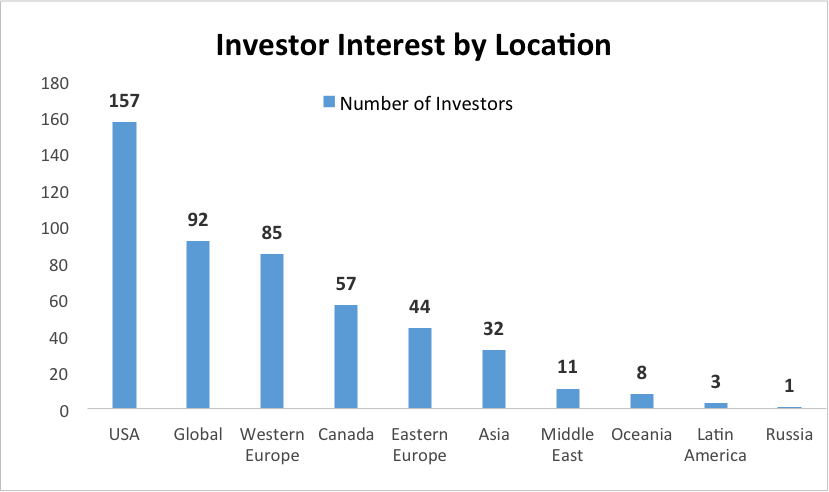

Having a validated list of potential investors is extremely valuable, and this process is usable by virtually any fundraising entrepreneur in the life science industry. The fact that investor and company fit is an extremely important precursor variable into building a successful relationship that could lead to an an allocation. is the reason why this process is valuable, and is a fact that LSN’s Research and Business Development staff have seen the value of fit proven in the marketplace time and time again. Through this process outlined above, the research team at LSN has been able to identify thousands of life science investors and our number of investor profiles is still growing.

If you wish to see the presentation slides, click here.