By Patrik Frei, CEO, Venture Valuations

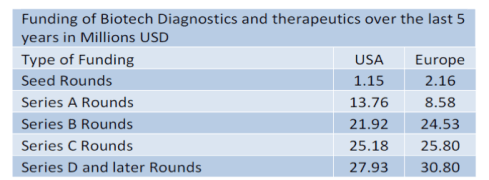

It is a common perception that privately-owned biotech firms seeking funding in the United States receive more money per round than their European counterparts. However, when comparing and analyzing the financing rounds of biotech companies working in the field of diagnostics and therapeutics for both geographies, it is clear that this is not the case. We looked at 156 financing rounds in Europe and 265 in the US over the past five years for biotech therapeutic and diagnostic companies, all of which are listed in the Life Science Nation database. For each data point, we had at least nine financing rounds.

The table below shows the average value by financing round in both the US and Europe over the last five years. In later financing rounds – especially series B, C, D and above – the average value is nearly identical in both the US and EU. We can see, from the table below that the largest variances in financing rounds come right at the beginning of the biotech’s life; in seed financing (61% higher in Europe) and Series A financing (46% lower in Europe).

Source: Life Science Nation

Source: Life Science Nation

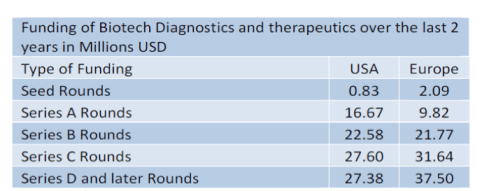

Looking at the table of just the last two years below, we can again see that the US does not receive more money compared to Europe. In fact, the difference between average financing rounds in the US and EU shrank for both series B and C financing. On the other hand, regional disparities for Seed and Series A financing becomes even more apparent. The percentage difference between seed rounds grows to 85% in Europe’s favor while the US widens the gap in series A financing up to 51%.

It should be mentioned that the gap in series D and later rounds also grew substantially in Europe’s favor. It is our opinion that this difference is largely due to outlier effects on a decreased sample size. In April of this year, Circassia, a biotech firm in the UK, closed a GBP 60 M (USD 98 M) series D round, significantly skewing the data set for Europe’s “Series D and later Rounds.”

Source: Life Science Nation

Source: Life Science Nation

We have seen that differences do exist between the US and EU when it comes to early stage funding – specifically, Seed and Series A financing rounds. But what causes these differences? We believe that one causes the other.

One reason for the differences between seed funding could be the increased availability of early-stage funding in Europe as opposed to the US. In A Comparison Between European and U.S. Venture Capital Industries, Vanessa Anderson and Frank Brinkhaus, PhD,cite initiatives such as the European Seventh Framework Programme (FP7) and Innovative Medicine Initiative (IMI) which combine to funnel up to USD 3.8 B into European small and medium sized biotechs, as resources that make funding more easily available. More angel investors and family offices may also allow European biotechs an easier time acquiring early stage funding while the US is left to finance through the three F’s (friends, family and fools). Additionally, there might be significantly different criteria for receiving funding between the US and EU. Since FP7 and IMI, as well as other initiatives, have the goal of fostering an emerging biotech industry in Europe, a comprehensive business plan and top-quality technology must be looked at alongside the potential for job creation and other economic stimulation when determining which firms will receive seed financing. Simply put, the focus is not always on what firm will have the greatest returns, but rather, where the greatest value is created for the economy as a whole. Secondly, the biotech industry is more mature in the US, and therefore, early investors have more experience determining value from business plans and early technology.

If it is the case – that funding for start-up capital is harder to come by in the US than it is in Europe – this may be the reason the US has higher A financing rounds. In the US, only those companies showing considerable promise, a unique technology, solid business plan, and extensive management capabilities and experience will receive the capital necessary to start-up their biotech. If only the most promising firms receive start up funding, there will be a “weeding out” effect, meaning only those most promising biotech firms will be seeking venture capital funding for Series A rounds. Financing is done in rounds to allow venture capitalists to see important milestones without having to commit all their money up front. This allows the VC’s to wait for less risk before they inject more money. If a US biotech firm is able to show an exceptional technology has been taken through the proof of concept stage, and the management has done it under considerable monetary constraints as opposed to its EU counterparts, VC’s should view this as a high up-side potential company with a decreased risk profile. Consequently, venture capitalists will be willing to invest more in a Series A rounds to own a larger share of the biotech company.

If you would like to get more information on the individual data points or search any of the over 3,000 financing rounds in the life sciences space, please have a look at the Life Science Nation database. http://www.lifesciencenation.com

Tags: Investors, letter, Life Science, news, newsletter

There is not enough capital to fund all of the good ideas from life science companies, which is a major challenge for life science CEOs today. To identify the next not-so-obvious investors, fundraising executives should look to the capital-raising practices of start-ups in other industries. If they do, they will learn that the basic premises include thinking outside the box and being flexible and more creative.

There is not enough capital to fund all of the good ideas from life science companies, which is a major challenge for life science CEOs today. To identify the next not-so-obvious investors, fundraising executives should look to the capital-raising practices of start-ups in other industries. If they do, they will learn that the basic premises include thinking outside the box and being flexible and more creative.