By Dennis Ford, CEO, LSN

The Good

I like crowdfunding for the life science arena because this industry already has a proven global audience that “votes with their feet” through a vast web of charitable platforms that raise money for research. Take, for instance, the crowds on any spring/summer weekend walking for this or that cure; the fact that everyone is in some way affected by disease makes these crowds not only readily available – but also relatively knowledgeable – potential investors.

Another unique value that these potential investors possess is that they emphatically want to change the world and help mankind. The fact is that almost everybody already donates in some capacity to research that aids in fighting disease, be it the extra dollar at grocery store checkouts or a planned donation to a charity or foundation. The question is whether or not crowdsourcing portals channel this worldwide source of capital in an adroit and compelling way. Basically, the net/net here is that crowd sourcing is already alive and well – and working. However, the biggest question is if the model can be transferred into the general population of potential investors made accessible by the jobs act, not just the accredited ones.

A side effect of this medium is that when you get onto the grid with your fundraising campaign, and are now in the mix and published, you are visible to everybody, which means an investor (or syndicate of investors) can come over the transom and write a big check and solve the fundraising issue by including you in a portfolio of life science assets.

So, the good is: it will work for launching a firm. However, you cannot raise over $1 million per year, and over $500k requires extensive filing and compliance, which can easily become an administrative headache.

The Bad

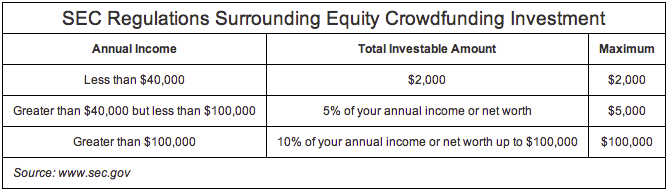

The main issue here is the numbers game that one has to play in order to reach a seven-figure goal, which translates to a large volume of required investors considering the SEC limits on investments in equity crowdfunding (see chart at the bottom of this article) – not to mention how to create dialogue and manage ongoing relationships with a group of investors of this size.

Crowdfunding is a paradigm shift. However, the ante into the game is where the biggest questions of all arise. Some sites are showing a very greedy edge, with equity positions ranging from 2 to 10+%, and/or a piece of the monies raised (between 5 -20%); that’s a pretty steep business model for a virtual company profile and a three minute video. As I look at the first batch of crowd sourcing portals and their associated business models, I am reminded of the Wild West and the stereotypical cast of characters. The mantras from the entrepreneurs who run these portals are pretty much all the same: “the risk to the investor is low because the investment dollar amount is low,” with the lofty slogan “the people will decide what makes its way into the market”.

Translating this into experimentally based life science technologies may be tricky, as the general public isn’t necessarily going to grok the subtleties of therapeutic biomarkers, or mechanisms of action, or physics-based, next-gen medical devices. The obvious candidates for this kind of funding, therefore, are easily understood healthcare IT solutions and/or simply comprehensible medical devices. The trick then for the therapeutic technologies is to take the high road, and use a similar easy-to-understand, high-level approach when pitching their technology.

Keeping it simple and using crowdfunding as a tactic for part of the strategy for early stage capital raising will be fine. However, it won’t be the full-blown solution to the industry’s capital needs.

The Ugly

How ugly can it be if you cannot see it yet, and where does crowd funding really fit? In my opinion, the fog has not been cleared on the regulatory side, and we have to wait for the rules and regulations to come down from on high. As of July 2013, no one knows what crowdfunding for equity investment currently really looks like!

I can speculate that because of the associated regulations, the best bet is as follows: if you need less than $500K to jump start your company, then you do not have to make the considerable investment of filing audited financial statements, which may also include compliance issues like keeping track of all communications through phone, email, and face-to-face meetings, etc., which translates to a very large administrative overhead.

The Bottom Line

The big challenge for the translational scientists is simplifying their message to a wider, less technically versed audience. Science needs to move through the experimental process step by step, and therefore, trying to get funding step by step is a reasonable approach if it is part of an overall fundraising strategy. What I mean by this is avoid the guardrail-to-guardrail, fits and starts approach, and have crowdfunding as a tactic in your overall strategy. Find small dollars to demonstrate efficacy, and then move on to the traditional groups and the new direct family offices and institutional investors for the larger capital needs.

At the end of the day, the scientist-entrepreneur has to understand that if he wants to play, he has to educate his or herself in the world of capital allocation, and the map that they use to do this has to be fresh and accurate and not dependent on the old models of fundraising, but rather reflect all the options, and how those options may map to the company’s needs over the next 5-7 years. The real take away from this discussion is that you need to create a strategy that covers all stages of your company’s financial needs by drawing the map of investor prospects for each stage.